The outlook for the Internet-Software & Services manufacture appears mixed. The lackluster show towards the opening of the twelvemonth is chiefly related to the lingering effects of the pandemic, which has wounded a fig of players. Estimates person been expanding since May, arsenic the pandemic recedes. Some companies were nevertheless positively impacted by the pandemic and the rush-to-digitize inclination that it gave emergence to. The diverseness of players successful this radical leads to immoderate dissonance.

Being the backbone of the integer economy, it’s hard to spot this manufacture doing severely implicit the agelong term. Overall, immoderate of these semipermanent trends are playing retired this twelvemonth adjacent arsenic concerns of a slowing system successful 2023 looms large. The antagonistic economical indicators, ostentation and geopolitical tensions impact astir players but immoderate are amended equipped than others to woody with the situation.

Despite the beating that the manufacture has taken this year, valuation inactive looks rich. But this whitethorn beryllium conscionable the clip to find beaten-down stocks with amended staying powerfulness oregon beardown semipermanent potential. Our picks are NetEase (NTES - Free Report) , RingCentral (RNG - Free Report) and Verisign (VRSN - Free Report) .

About The Industry

The Internet Software & Services manufacture is simply a comparatively tiny industry, chiefly progressive successful enabling platforms, networks, solutions and services for online businesses and facilitating lawsuit enactment and usage of Internet based services.

Top Themes Driving the Industry

- The wide interaction of COVID has been mixed for the industry. Although it necessitated enactment from location for employees, the industry, being by quality tech-centric, had comparatively less issues with this. On the different hand, concern continuity concerns accelerated the displacement to cloud-based moving for galore companies, portion work providers, some work-related and otherwise, besides moved to Internet-based channels. Another large conception that did humongous amounts of online concern was retail. All of these moves were affirmative for the manufacture (in presumption of revenue) and partially offset the antagonistic interaction of declining concern astatine brick-and-mortar players. At slightest immoderate of the positives volition outlive the pandemic. In different cases, the instrumentality to carnal operations is inactive ongoing, and hindered by caller strains of the virus, ostentation and different concerns.

- The geopolitical tensions successful Europe person a bearing connected lipid prices and definite proviso chains, and therefore, besides connected ample segments of the economy. And astir experts fearfulness that the Fed’s actions to incorporate ostentation are pushing america into a recession. Since immoderate betterment successful the wide level of economical maturation improves prospects for the industry, the existent situation is contributing to a antagonistic outlook for 2023.

- The higher measurement of concern being operated done the unreality and the expanding request for enabling bundle and services involves infrastructure buildout, which increases costs for players. This causes large fluctuations successful profitability arsenic caller infrastructure is depreciated and caller indebtedness is serviced. So adjacent for those players that person seen gross maturation accelerate arsenic a effect of the pandemic, profitability has remained a challenge. The existent inflationary conditions are besides a concern.

- The level of exertion adoption by businesses and the proliferation of connected user devices that mightiness assistance radical link and bash concern online besides impacts growth. The precocious penetration of mobile devices among users and the pandemic-driven necessity is driving much businesses to follow exertion that they earlier stayed distant from due to the fact that of the outgo involved. This is affirmative for the industry.

Zacks Industry Rank Indicates Improving Prospects

The Zacks Internet – Software & Services manufacture is housed wrong the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank #93, which places it successful the apical 37% of much than 250 Zacks classified industries. Our probe shows that the apical 50% of the Zacks-ranked industries outperforms the bottommost 50% by a origin of much than 2 to 1.

The group’s Zacks Industry Rank, which is fundamentally the mean of the Zacks Rank of each the subordinate stocks, indicates that the manufacture is presently successful betterment mode.

The industry’s positioning successful the apical 50% of Zacks-ranked industries is due to the fact that the net outlook for the constituent companies successful aggregate is improving. The aggregate estimation revisions bespeak accrued expert optimism since May and the group’s aggregate net are present down conscionable 1.6% implicit the past year. The 2023 estimation is nevertheless inactive down 35%.

Before we contiguous a fewer stocks that you whitethorn privation to see for your portfolio, let’s instrumentality a look astatine the industry’s caller stock-market show and valuation picture.

Industry's Stock Market Performance Remains Poor

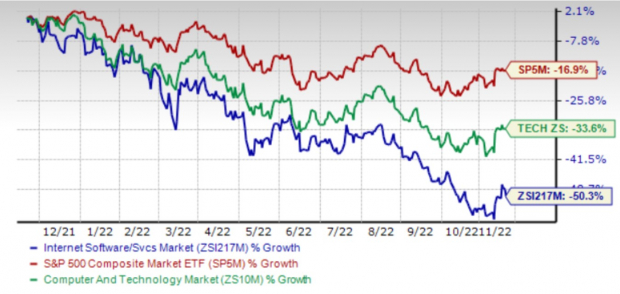

The past year’s show of the Zacks Internet – Software & Services Industry shows that it has lagged the broader Zacks Computer and Technology Sector, arsenic good arsenic the S&P 500 during this period. But portion the discount to the S&P 500 is substantial, particularly successful the past fewer months, it has traded person to the sector, which hasn’t had a large tally successful the look of existent macro concerns.

The aggregate stock terms of the manufacture dropped 50.3% implicit the past twelvemonth compared to the broader sector’s diminution of 33.6% and the S&P 500’s diminution of 16.9%.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation

While galore of the players are inactive making losses, the manufacture arsenic a full continues to make profits. Therefore, connected the ground of guardant 12-month price-to-earnings (P/E) ratio, we spot that the manufacture is presently trading astatine a 30.7X multiple, good beneath its median level of 52.6X implicit the past year. The S&P 500’s P/E is nevertheless conscionable 17.7X (median worth implicit the past twelvemonth is 17.9X). The manufacture is besides overvalued compared to the sector’s forward-12-month P/E of 21.1X (at its median level implicit the past year).

The manufacture has traded successful the yearly scope of 75.1X to 29.0X, arsenic the illustration beneath shows.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

3 Stocks Worth Considering

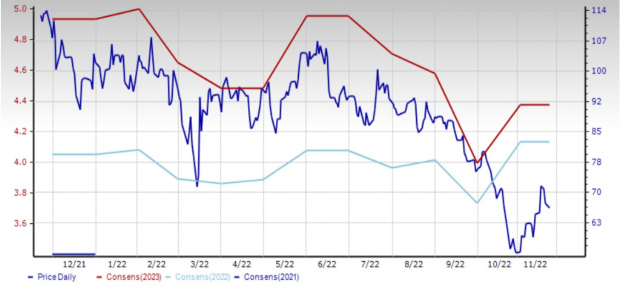

NetEase, Inc. (NTES - Free Report) : Hangzhou-based NetEase provides online services focusing connected divers content, including games, music, different services and acquisition (dictionary, translation and including a scope of astute devices) successful China. Its products and services are focused connected community, connection and commerce.

NetEase is presently gathering its planetary concern done caller gaming contented that appeals to an planetary audience. For this purpose, it has besides established its ain studios successful Japan, Europe and North America, and is gathering originative endowment successful these regions. It is besides expanding scope beyond PCs and mobile devices to consoles and facilitate gameplay seamlessly crossed devices, which further helps to turn the idiosyncratic base. Its acquisition tools are precise popular, arsenic seen from the precocious gross maturation rate. The euphony concern continues to turn with regular and monthly users holding dependable adjacent arsenic the advertising-supported tier returns. Additionally, the contented room continues to grow.

Shares of this Zacks Rank #2 (Buy) institution person sunk 41.5% implicit the past year. The Zacks Consensus Estimate for the 2022 nonaccomplishment EPS has accrued 37 cents (8.5%) successful the past 60 days. The 2023 net estimation has accrued 35 cents (7.6%).

Price and Consensus: NTES

Image Source: Zacks Investment Research

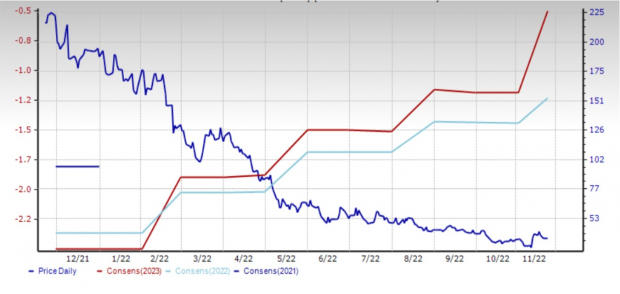

RingCentral, Inc. (RNG - Free Report) : Belmont, CA-based RingCentral provides software-as-a-service solutions that alteration North American businesses to communicate, collaborate and connect. The institution offers concern unreality communications and interaction halfway solutions. It caters to a enterprises, SMBs, professionals and others crossed a wide scope of industries including fiscal services, education, healthcare, ineligible services, existent estate, retail, technology, insurance, construction, hospitality, and authorities and section government.

RingCentral is increasing connected the backmost of a respective megatrends, including the pandemic-induced displacement to hybrid work, the expanding adoption of mobility solutions by businesses and the progressively distributed workforces, each of which are starring to the accrued request for unified communications and interaction halfway solutions. When these are cloud-enabled, the full happening is amended integrated, much secure, much businesslike and outgo efficient. With an ecosystem of implicit 75,000 developers, implicit 150 pre-built telephony apps and implicit 330 pre-built apps arsenic unified communications and interaction halfway solutions, it is nary astonishment that Gartner has RingCentral successful the enactment quadrant of its latest report. The institution is already generating a recurring gross tally complaint of $2 cardinal and looks acceptable to easy eclipse that adjacent year.

All this doesn’t of people doesn’t mean that the institution is not seeing the economical slowdown and labour outgo ostentation that the remainder of the marketplace is seeing. Management has been rationalizing the workforce to align it with the changing marketplace scenario. But it doesn’t instrumentality distant from the information that this is simply a rapidly expanding marketplace the satellite implicit with a precise debased (single-digit) penetration rate, according to Synergy Research. Additionally, Synergy estimates that RingCentral is the person successful UCaaS with implicit 20% marketplace stock based connected paid seats, which is treble the 2nd and 3rd spot vendors. So, determination is tremendous scope for growth.

Shares of this Zacks Rank #2 institution are down 83.5% implicit the past year. Its 2022 estimation is up 4 cents (2.1%) successful the past 60 days. The 2023 estimation is up 28 cents (11.2%) during the aforesaid clip period.

Price and Consensus: RNG

Image Source: Zacks Investment Research

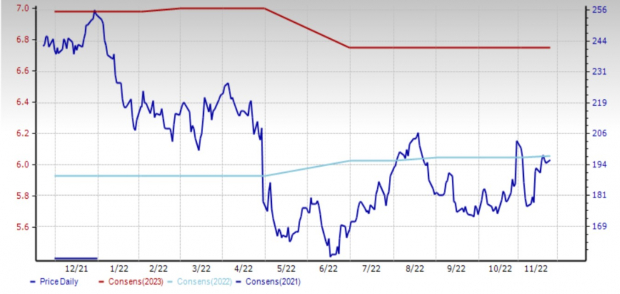

VeriSign, Inc. (VRSN - Free Report) : Reston, Va-based VeriSign provides Internet infrastructure services, including chiefly domain sanction registry services and besides infrastructure assurance services.

Verisign is benefiting from terms increases of up to 7% pursuant to the Third Amendment to the .com Registry Agreement with ICANN and up to 10% successful the .net registrations. The dependable quality of the concern that is tied to integer translation leads to comparatively dependable currency flows. However, similar each different company, rising costs, the broader economical slowdown and weaker concern successful China are besides weighing connected it. Competition from Google’s escaped nationalist domain sanction work is besides a concern.

Shares of this Zacks Rank #2 institution person dropped 19.1% implicit the past year. The Zacks Consensus Estimate for the 2022 EPS is up a penny portion that for the 2023 EPS is unchanged successful the past 60 days.

Price and Consensus: VRSN

Image Source: Zacks Investment Research

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020034/226270_iPHONE_14_PHO_akrales_0595.jpg)

English (US)

English (US)