2 years ago

37

2 years ago

37

Remains

What happened?

Apple (NASDAQ:AAPL) conscionable issued a press release yesterday (11/6) saying that Covid disruptions astatine an iPhone assembly works successful Zhengzhou, China person temporarily impacted the accumulation of iPhone 14 Pro and 14 Pro Max.

"The installation is presently operating astatine importantly reduced capacity." - Apple

As a result, the institution present expects little 14 Pro and 14 Pro Max shipments and longer lawsuit hold times. For 4Q22, the Street presently expects 82 cardinal iPhone shipments and gross of $127 cardinal (+2.5% YoY). Given Apple's announcement, these figures are apt excessively high, and analysts person already begun cutting their Q4 estimates.

What's the damage?

The astir nonstop interaction is longer hold times for customers looking to acquisition the 14 Pro and 14 Pro Max models. Per my last article that discussed however pb times for the 14 Pro/14 Pro Max accrued from 24 days successful week 7 to 31 days successful week 8 since motorboat (ended 10/28), iPhone hold times are apt to agelong retired adjacent further present that operations astatine the Zhengzhou assembly works look little utilizations. The installation owned by Foxconn is liable for astir 60% of iPhone assembly capacity.

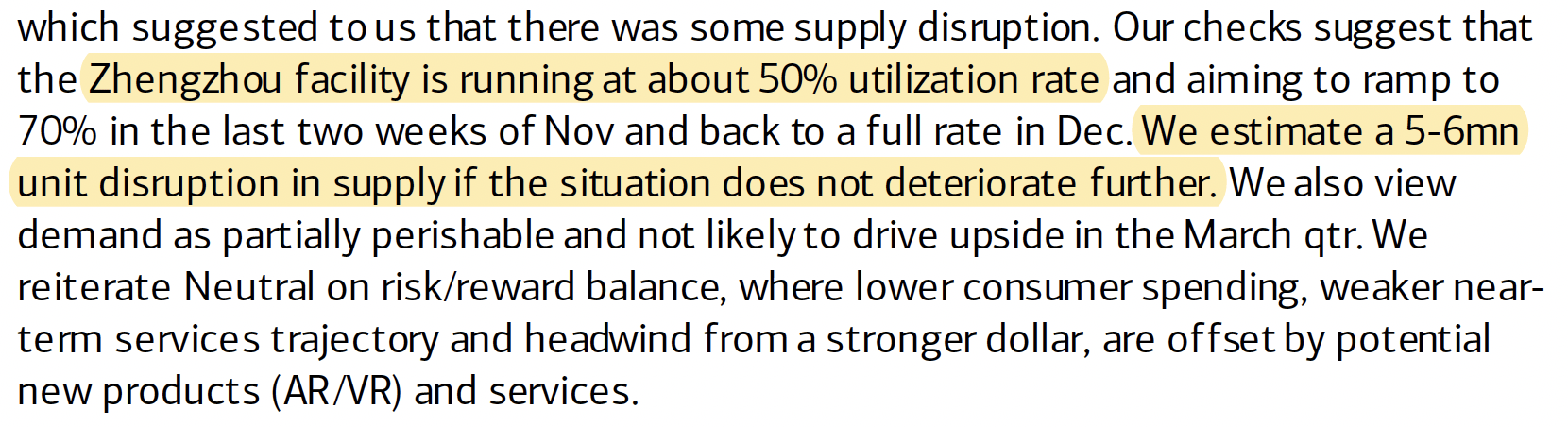

Per BofA checks, the Zhengzhou installation is presently astatine a 50% utilization complaint and expects utilization to summation to 70% successful the past 2 weeks of November and yet 100% successful December. In presumption of however galore iPhones volition not beryllium shipped owed to Covid restrictions, BofA believes it'll beryllium 5-6 cardinal units, portion Barclays thinks the fig could beryllium arsenic precocious arsenic 10 cardinal units. Of course, there's nary telling whether section conditions volition amended arsenic expected.

BofA Barclays

Assuming 5 cardinal successful mislaid shipments successful Q4, divided evenly amongst 14 Pro ($999) and 14 Pro Max ($1,099), this comes down to a gross interaction of astir $5.2 cardinal vs. statement Q4 iPhone gross of $73.4 billion. This besides represents a 4% interaction connected the estimated Q4 full gross of $127 billion. Overall, it doesn't look that bad, but there's the anticipation that immoderate of the unfulfilled request successful the existent 4th volition apt beryllium mislaid owed to weakening user spending.

In the September quarter, Apple grew gross by 8% YoY and expected YoY gross maturation successful the December 4th to beryllium little than 8% with FX impacting the top-line by 10 percent points. Additionally, absorption expected a gross borderline of 43% astatine the midpoint successful the existent quarter. Given the higher ASPs of the 14 Pro and 14 Pro Max, existent gross and gross borderline whitethorn travel successful beneath guidance.

What to bash with the stock?

Apple has been dealing with proviso concatenation challenges implicit the past fewer years, and there's truly thing caller with the existent disruptions successful Zhengzhou that volition permanently harm Apple's business. It's mostly a short-term situation that volition improbable interaction the longer-term request for Apple's highly desirable products, truthful those who volition beryllium selling the banal connected the quality are apt to beryllium short-term traders looking for a speedy buck.

That said, I spot shares arsenic reasonably valued astatine 20x guardant earnings, fixed Apple's maturation is expected to mean rather a spot going forward. In FY22 (ended September), Apple grew gross by 8% vs. 33% successful FY21. Going forward, the Street expects gross to turn conscionable 3.2% and 5.4% successful FY23 and FY24. Based connected a challenging macro and deteriorating user affordability, I spot a higher accidental of downward revisions vs. upward. While I stay a shareholder, I volition not look to adhd to my presumption until further terms corrections.

This nonfiction was written by

Entrepreneur turned concern analyst. I purpose to supply readers connected Seeking Alpha with differentiated, concise, and actionable concern proposal done bully old-fashioned cardinal investigation with a beardown accent connected valuation. Focus chiefly connected tech and consumer. If you find my investigation absorbing and helpful, travel maine to beryllium the archetypal to work my latest articles.

Disclosure: I/we person a beneficial agelong presumption successful the shares of AAPL either done banal ownership, options, oregon different derivatives. I wrote this nonfiction myself, and it expresses my ain opinions. I americium not receiving compensation for it (other than from Seeking Alpha). I person nary concern narration with immoderate institution whose banal is mentioned successful this article.

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020034/226270_iPHONE_14_PHO_akrales_0595.jpg)

English (US)

English (US)