2 years ago

35

2 years ago

35

South_agency

Apple Inc. (NASDAQ:AAPL) designs, manufactures, and markets smartphones, idiosyncratic computers, tablets, wearables, and accessories worldwide. In July 2022, we published an nonfiction connected Seeking Alpha, titled: "3 Reasons Why We Think Apple Could Be Attractive At Current Valuations" and we rated Apple's banal arsenic "buy".

The reasons for our bargain standing were:

- Apple has performed historically good during times of debased user confidence, owed to its loyal lawsuit base, its beardown marque recognition, and its diversified merchandise portfolio.

- Easing of COVID-19 restrictions successful China whitethorn substance request maturation successful the future.

- Strong way grounds of paying harmless and sustainable quarterly dividends, portion the steadfast has besides purchased backmost a important information of its shares.

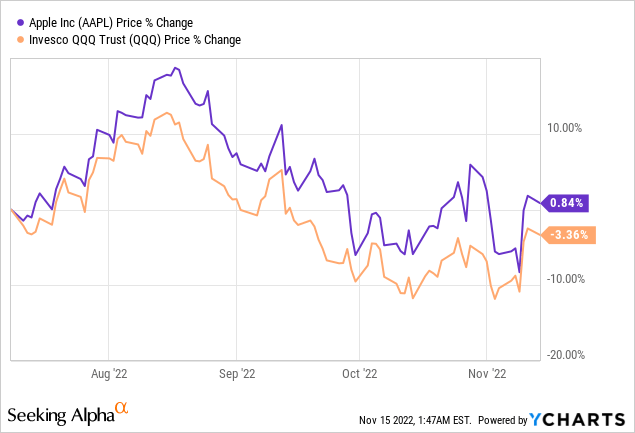

Since our past writing, Apple's banal terms has remained comparatively flat, however, it somewhat outperformed the QQQ.

Data by YCharts

Data by YCharts

Today, we person decided to revisit our investigation connected Apple, arsenic determination person been important developments precocious related to the manufacturing capabilities of the firm, particularly related to the operations successful China. Also, our erstwhile constituent related to the easing Covid restrictions successful China whitethorn not beryllium valid anymore. In this article, we are going to springiness an updated view, wherefore we inactive judge that Apple's banal could beryllium a bully bargain today.

But, fto america archetypal commencement with the caller developments.

Recent developments

The caller developments that we are going to absorption connected present are the ones related to Apple's accumulation capabilities successful China. Important to recognize that accumulation capableness successful China is chiefly influenced by governmental decisions related to containing Covid-19 outbreaks and not by method limitations.

Last month, Chinese President Xi has reiterated his volition to support the country's zero Covid argumentation successful place. This improvement has 2 imaginable impacts connected Apple's business:

1.) Demand for Apple's products whitethorn not turn arsenic accelerated arsenic expected, owed to imaginable lockdowns.

2.) Production of Apple devices whitethorn beryllium wounded owed to imaginable mill shutdowns.

In fact, the 2nd constituent has already materialized to a definite extent. Earlier successful November, the largest iPhone manufacturing works has been taxable to Covid-19 restrictions. Foxconn is liable for the accumulation of 70% of iPhones globally. It besides assembles devices successful India, but its Zhengzhou mill builds the largest portion of its planetary output. In the Zhengzhou complex, 200,000 employees enactment and live, arsenic it contains besides a dormitory, which enables workers to unrecorded astatine their workplaces. The purpose of this strategy is to bounds extracurricular interaction and trim the likelihood of Covid outbreaks. This measurement nevertheless did not entreaty to the workers, and thousands were trying to flee the facilities.

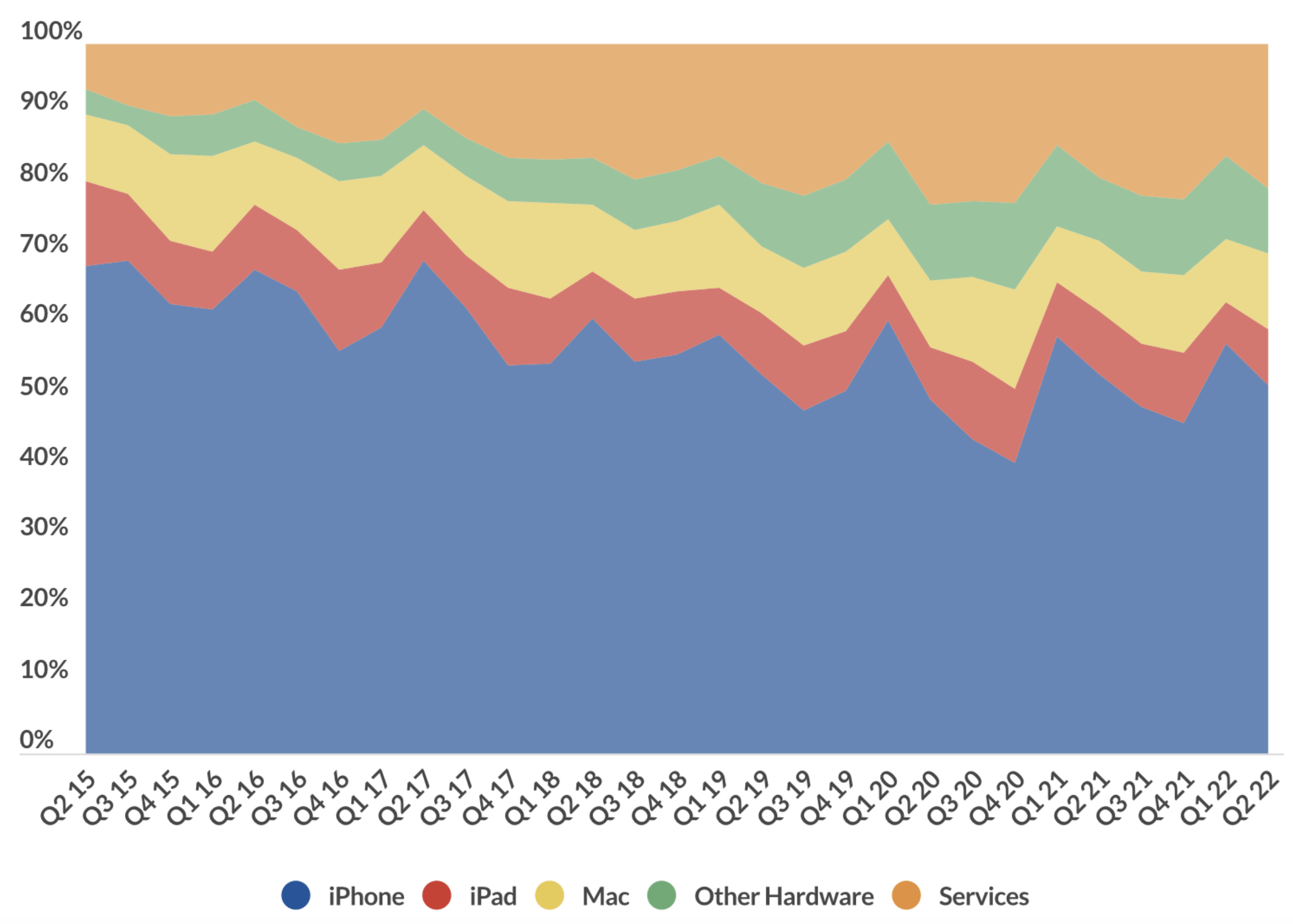

In our opinion, it is cardinal that the accumulation of iPhones remains uninterrupted arsenic this merchandise accounts for much than 50% of Apple's full revenue.

Revenue by root (businessofapps.com)

While the information of gross has been gradually decreasing implicit clip (which we judge is beneficial), it inactive makes up a precise important percentage. Any interruption to iPhone manufacturing oregon declining iPhone request could person a worldly interaction connected the firm's fiscal results.

Several analysts and Apple themselves person already acknowledged the antagonistic impacts of the lockdowns successful China. Earlier successful November, Apple announced that their iPhone shipments volition beryllium little than antecedently thought. They "now expect little iPhone 14 Pro and iPhone 14 Pro Max shipments than we antecedently anticipated, and customers volition acquisition longer hold times to person their caller products".

J.P. Morgan has besides lowered the forecast for iPhone shipments successful the December quarter. This lowered forecast would effect successful a declining gross year-over-over.

We judge that successful the adjacent future, arsenic agelong arsenic the Chinese Covid policies are successful place, specified quality tin person a worldly interaction connected Apple's concern and its stock price. The stock terms has shown a important absorption to each of the above-mentioned news.

So wherefore are we inactive optimistic?

First of all, contempt the pugnacious economical environment, the request for Apple products remains high, owed to the exceptional lawsuit loyalty. In our opinion, arsenic agelong arsenic the request is there, Apple volition beryllium capable to find a mode to proviso capable products. In fact, they are already moving connected moving distant a important information of the iPhone accumulation from China to India, which has much tenable Covid policies. We spot this arsenic an accidental successful the agelong term, arsenic Apple is present forced to diversify its manufacturing, which whitethorn effect successful a overmuch much robust concern and proviso concatenation successful the future.

What is precisely being done by Apple and Foxconn?

Apple has partnered with a Taiwan-based firm, called Pegatron, to manufacture iPhones successful India, successful an effort to trim the dependency connected China. This mill volition beryllium focusing connected making iPhone 14 and iPhone 12 models primarily.

On the different hand, Foxconn has besides started a important enlargement of its manufacturing capabilities successful India. The steadfast announced that they are readying to rise the workforce by arsenic overmuch arsenic 4 times successful the coming 2 years. With this move, the fig of workers would scope 70,000 successful Tamil Nadu successful India, which is inactive substantially little than the 200,000 employed successful Zhengzhou.

Further, Foxconn has announced that they person been moving connected tweaking the accumulation successful bid to conscionable the request for the vacation season.

Moving distant from China, however, is not a quick process. J.P. Morgan suggested Apple whitethorn beryllium capable to displacement astir 25% of its iPhone accumulation to India by 2025 and anticipated 5% of its iPhone accumulation this twelvemonth to determination to the country.

All successful all, we judge that Apple and its suppliers are making important efforts to support satisfying the request for iPhones and different Apple products astir the world, contempt the Covid related disruptions successful China. Investors indispensable support successful caput nevertheless that moving distant from Chinese manufacturing whitethorn instrumentality years, and the roadworthy to reaching the last extremity is apt to beryllium bumpy.

The determination distant from China is nevertheless not the lone origin that could amended Apple's fiscal show successful the agelong term.

Increasing gross from services

In Apple's latest earnings results, we tin spot a double-digit maturation of yearly gross successful the "Services" category.

Net income (million dollars) by class (Apple)

This summation has been chiefly driven by the expanding gross from advertising, unreality services, and the App Store. While the maturation has slowed from 27% to 14%, we judge that it is chiefly caused by the existent macroeconomic environment, and it is apt to beryllium temporary. Revenue from advertizing and the App Store is apt to beryllium straight impacted by the mediocre user sentiment observed successful the United States and astir the globe.

But wherefore bash we attraction truthful overmuch astir the maturation of the services segment?

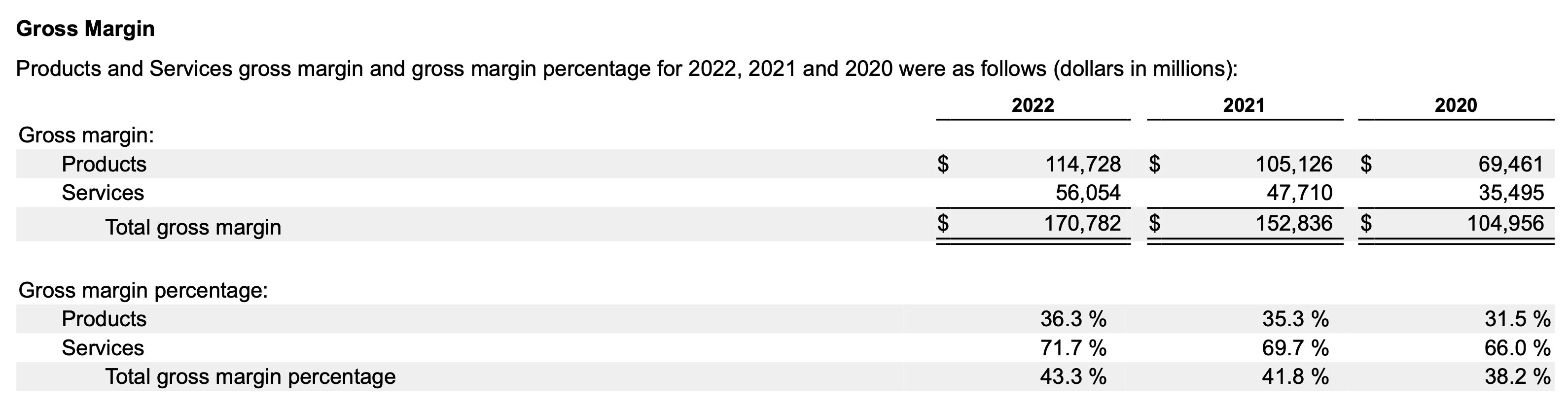

Because the "Services" conception has the highest gross margin.

Gross borderline (Apple)

While products person had gross margins betwixt 31-37%, "Services" person had a importantly higher scope of 66-72%, gradually expanding each twelvemonth successful the past 3 years. With expanding gross from the "Services" category, we expect the full gross borderline to expand, resulting successful an summation successful nett income successful the agelong run, which could perchance unlock important worth for the investors.

Valuation

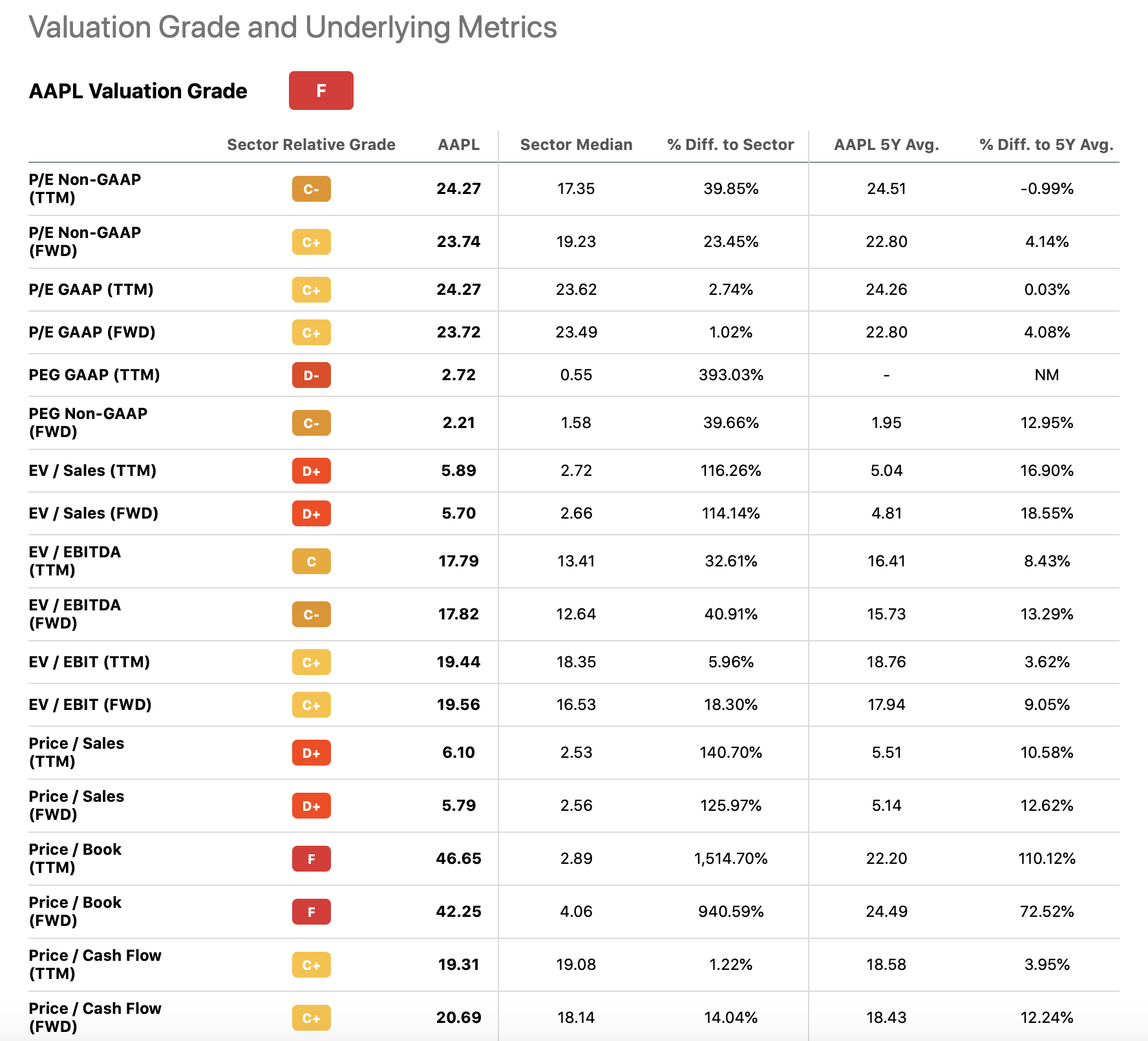

According to the accepted terms multiples, Apple is trading astatine a valuation substantially supra the assemblage median.

Valuation (Seeking Alpha)

On the different hand, the existent multiples are astir successful enactment with the firm's ain 5Y averages.

In our opinion, the existent premium to the assemblage median is justified. The gradual determination distant from Chinese manufacturing and the expanding gross from the "Services" conception are each factors that we judge volition marque Apple's concern much robust successful the agelong term, adjacent if near-term headwinds related to the macroeconomic situation are slowing their maturation now.

Key takeaways

China's Covid argumentation has a important interaction connected some the proviso and request for iPhones. Recently, the largest iPhone manufacturing analyzable successful China has been enactment nether lockdown, which is apt to origin the iPhone output for the December 4th to beryllium substantially beneath expectations, starring to a year-over-year gross decline.

On the different hand, Apple and its partners and suppliers are moving hard to trim the dependency connected the manufacturing successful China. Foxconn has announced a important workforce maturation successful India during the coming 2 years, portion Apple has further strengthened its concern with Pegatron to summation iPhone accumulation volumes.

While we judge that Apple's banal terms whitethorn beryllium volatile owed to the Covid-related quality successful the adjacent term, we expect the steadfast to payment from the existent developments successful the agelong term. Also, the gradually declining dependency connected iPhone income successful presumption of gross and the expanding gross from the "Services" class is simply a bully sign, successful our view.

The steadfast is presently trading astatine terms multiples adjacent to its 5-years averages and the respective assemblage medians. We judge that this valuation is justified, and we support our "buy" standing connected Apple.

This nonfiction was written by

Petroleum technologist with an enthusiasm for investing, accounting and idiosyncratic finances.

Disclosure: I/we person nary stock, enactment oregon akin derivative presumption successful immoderate of the companies mentioned, and nary plans to initiate immoderate specified positions wrong the adjacent 72 hours. I wrote this nonfiction myself, and it expresses my ain opinions. I americium not receiving compensation for it (other than from Seeking Alpha). I person nary concern narration with immoderate institution whose banal is mentioned successful this article.

Additional disclosure: Past show is not an indicator of aboriginal performance. This station is illustrative and acquisition and is not a circumstantial connection of products oregon services oregon fiscal advice. Information successful this nonfiction is not an connection to bargain oregon sell, oregon a solicitation of immoderate connection to bargain oregon merchantability the securities mentioned herein. Information presented is believed to beryllium factual and up-to-date, but we bash not warrant its accuracy and it should not beryllium regarded arsenic a implicit investigation of the subjects discussed. Expressions of sentiment bespeak the judgement of the authors arsenic of the day of work and are taxable to change. This nonfiction has been co-authored by Mark Lakos.

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020034/226270_iPHONE_14_PHO_akrales_0595.jpg)

English (US)

English (US)