.png) 2 years ago

53

2 years ago

53

Justin Sullivan

Meta Platforms' (NASDAQ:META) Family of Apps ('FOA') Facebook, Instagram, and WhatsApp inactive boast coagulated engagement and improving monetization prospects, beardown web effects, and robust escaped currency travel generation. Add progressively compelling valuation and the stock's entreaty seems irresistible.

Still, a caller diminution successful gross and nett income, the emergence of almighty rivals (TikTok, not to notation Amazon (AMZN), Apple (AAPL), and Microsoft (MSFT)), awesome an erosion of marketplace moat and alteration successful fortune, prompting CEO Mark Zuckerberg to question renewal.

The planetary metaverse marketplace size is expected to turn astatine a compound yearly maturation complaint ('CAGR') of 39.8% during 2022-2030. Reality Labs is simply a stake connected the instauration of an ecosystem that encapsulates AI, AR, Virtual Reality alongside 3D, blockchain, virtual worlds/games, online shopping, wherefore not hunt and iPhone-rival functionality.

Nothing abbreviated of manufacture 4-type tech, and perchance close backmost astatine Apple. Willingly oregon not, Apple started a warfare with its App Tracking Transparency (ATT) implementation; present it's astir to spot the combatant - and get a tally for the money. Even Microsoft scents the blood.

Recent Quarterly Results Don't Spell the End, Just a New Beginning

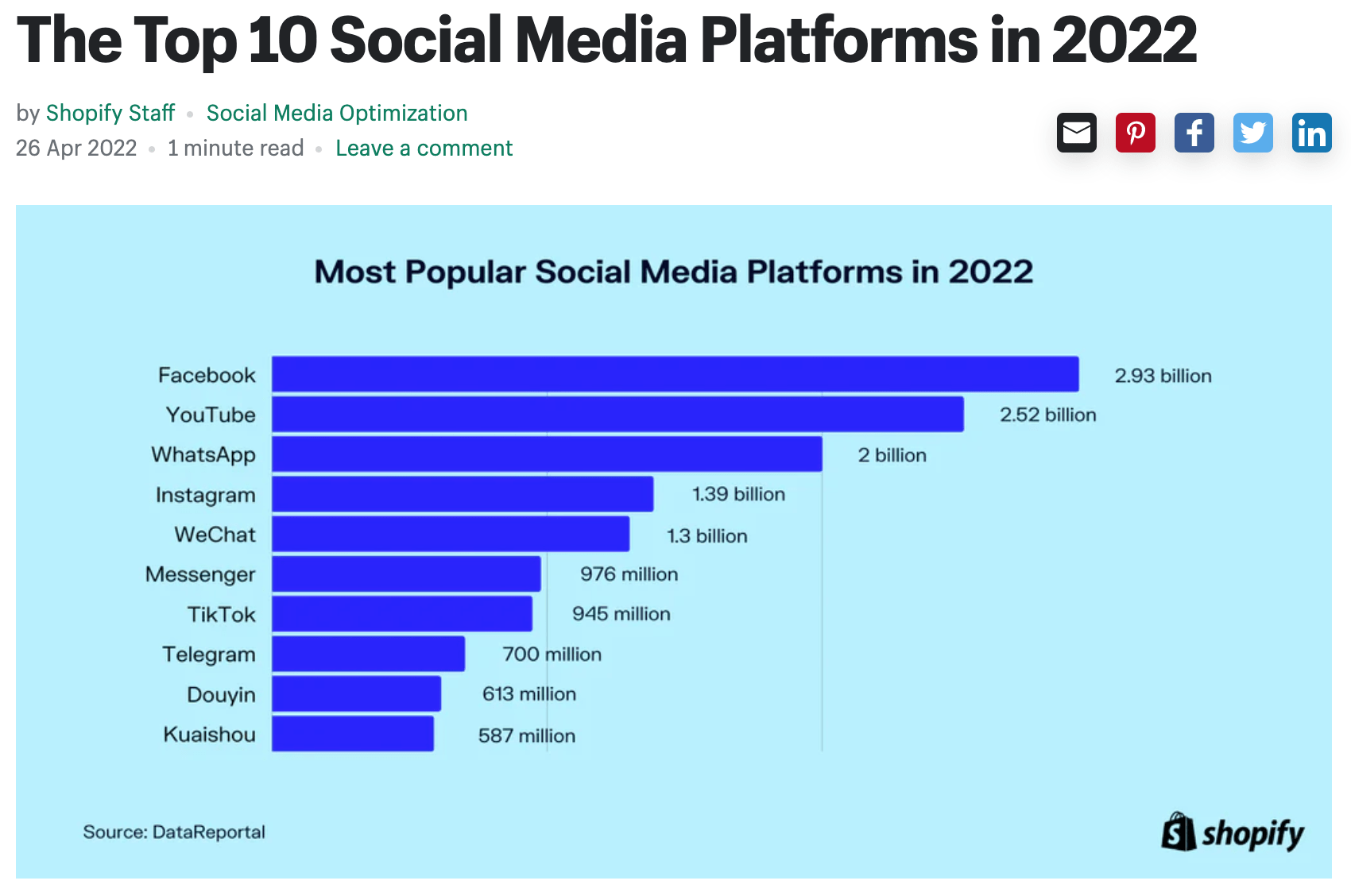

The banal fell hard pursuing work of the firm's Third Quarter 2022 Operational and Other Financial Highlights. But Family daily/monthly progressive radical were 2.93 cardinal and 3.71 cardinal respectively for September 2022, an summation of 4% year-over-year. Facebook regular and monthly progressive users were 1.98 cardinal and 2.96 billion, besides bully for a flimsy summation year-over-year. Engagement frankincense remains strong. So overmuch for the assertion that Meta's FOA's idiosyncratic basal is evaporating and the steadfast loses traction successful the marketplace. It's conscionable pugnacious to turn treble digits disconnected specified a ample base. The institution does inactive predominate the satellite of societal media. For each the chat astir TikTok, the rival is inactive lone 1 3rd the size of Facebook and fractional the size of WhatsApp, arsenic is made wide below.

DataReportal

In the 3rd 4th of 2022, advertisement impressions delivered crossed Family of Apps accrued by 17% year-over-year. Not atrocious astatine all.

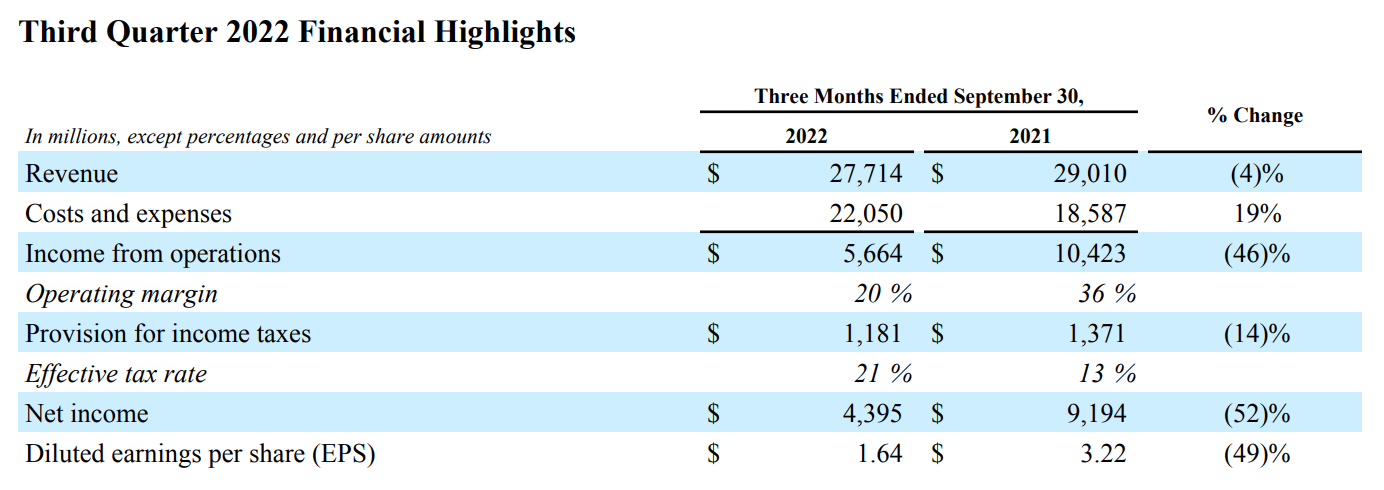

Now for wherever it hurts the most. Q3 '22 Revenue was $27.71 billion, a alteration of 4% year-over-year, but it's inactive an summation of 2% connected a changeless currency basis. As Management was speedy to constituent out, "had overseas speech rates remained changeless with the 3rd 4th of 2021, gross would person been $1.79 cardinal higher". Total costs and expenses were $22.05 billion, an summation of 19% year-over-year - not good, but this includes an impairment nonaccomplishment of $413 cardinal for operating leases. No wonderment Meta's laying disconnected immoderate of its unit and the banal rallied 2 days agone successful an different grim marketplace connected the imaginable of important resulting operating expenses reductions, signaling Management's committedness to its shareholder basal - and profitability. (Meta besides repurchased $6.55 cardinal of its Class A communal banal successful the 3rd 4th of 2022. As of September 30, 2022, the steadfast had $17.78 cardinal disposable and authorized for repurchases; astatine Meta, shareholders bash matter, Zuckerberg is 1 aft all.)

Capital expenditures, including main payments connected concern leases, were $9.52 cardinal for the 3rd 4th of 2022, a important summation from $7.75 cardinal for the 2nd 4th of 2022. But Cash, currency equivalents, and marketable securities managed to beryllium $41.78 cardinal arsenic of September 30, 2022, really higher than $40.49 cardinal arsenic of June 30, 2022. Long-term indebtedness was $9.92 billion.

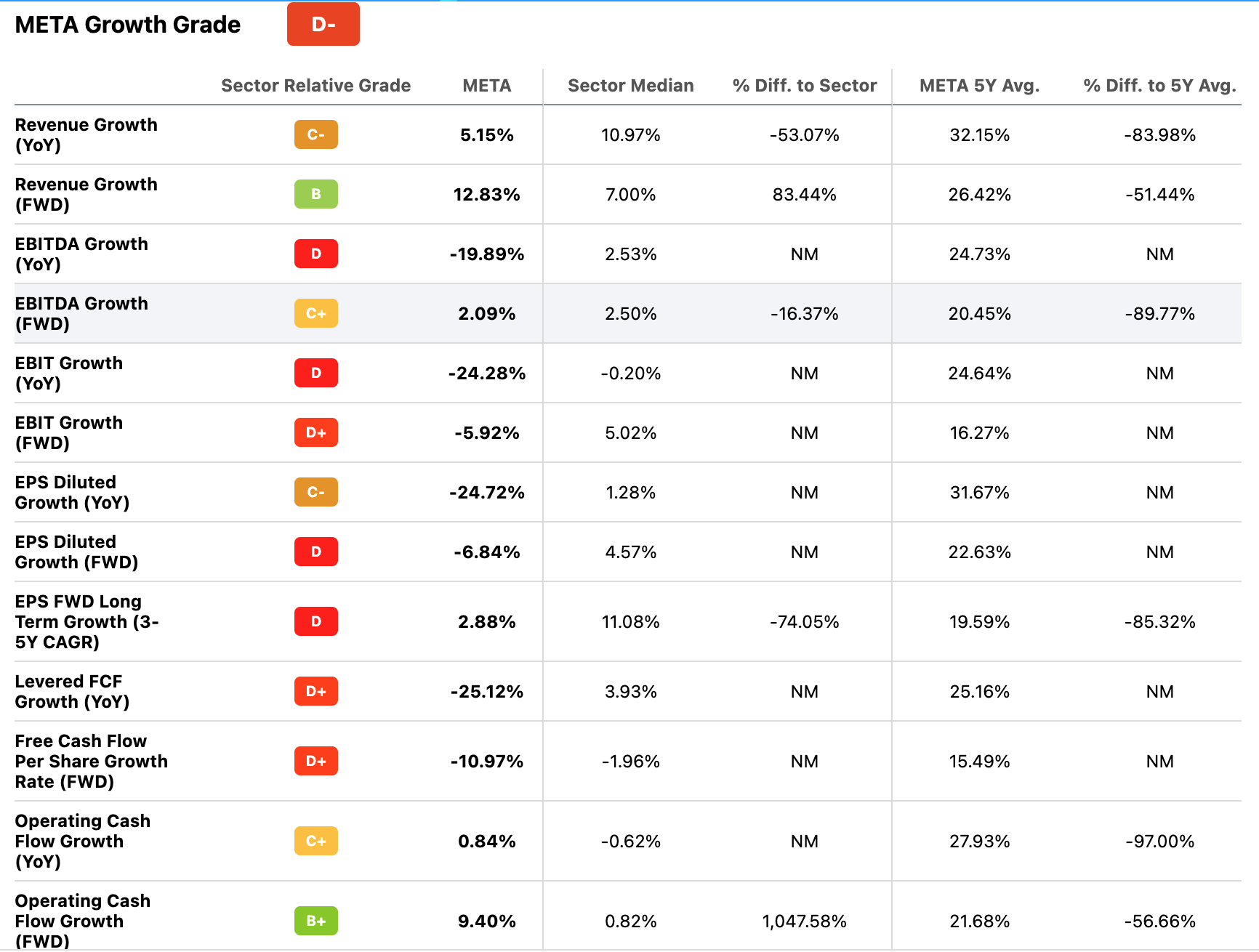

The aforementioned gross diminution guides Meta's mediocre maturation grade, arsenic follows:

Seeking Alpha

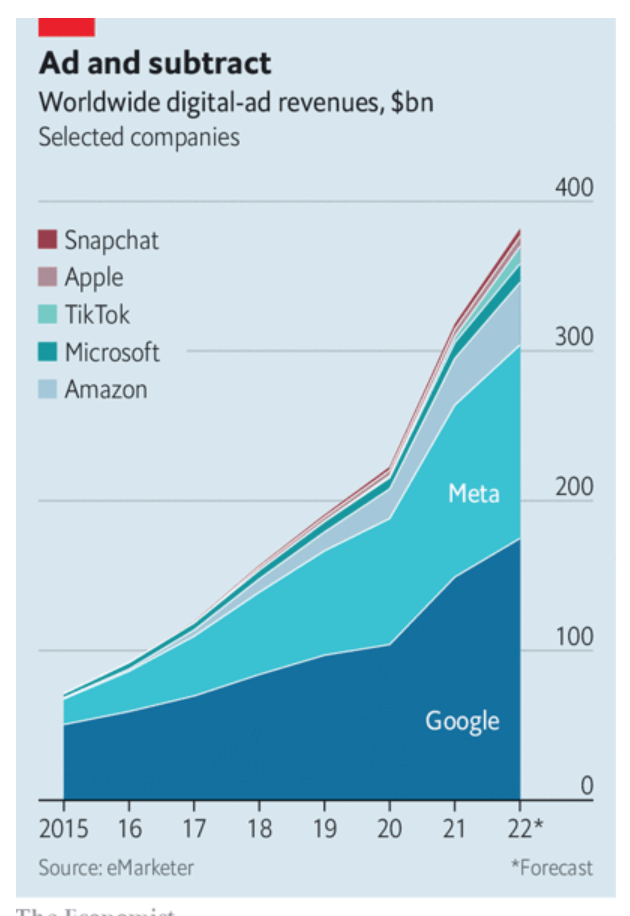

Driving the erosion of Meta's apical enactment are a slowing system (with the enslaved marketplace present considering a recession successful 2023 a 100% certainty), which results successful a slowdown successful digital-ad revenues, Apple's App Tracking Transparency implementation, and intensifying competition, peculiarly from Amazon and, of course, Alphabet's Google (GOOG) (GOOGL). The emergence of different cardinal players including ByteDance's TikTok, Microsoft's LinkedIn, Apple, Netflix's (NFLX) ad-subsidized streaming work (just getting started), is further complicating the outlook (see beneath for detail).

eMarketer

Still, Meta expects 4th fourth 2022 full gross to beryllium successful the scope of $30-32.5 billion, frankincense astir 10% higher. This guidance assumes overseas currency volition beryllium an astir 7% headwind to year-over-year full gross growth, based connected existent speech rates. Not precisely the extremity of the world.

What apt wounded the banal the astir pursuing quarterly results is losses incurred launching Reality Labs.

Per Meta's Third Quarter 2022 Results report (i.e., CFO Outlook Commentary):

We expect the flimsy bulk of our 2023 disbursal dollar maturation to beryllium driven by operating expenses, with the remaining maturation coming from outgo of revenue. We expect the percent maturation complaint of 2023 operating expenses to decelerate meaningfully arsenic we curtail non-headcount related disbursal maturation (...). Conversely, our maturation successful outgo of gross is expected to accelerate, driven by infrastructure-related expenses and, to a lesser extent, Reality Labs hardware costs driven by the motorboat of our adjacent procreation of our user Quest headset aboriginal adjacent year. Reality Labs expenses are included successful our full disbursal guidance. We bash expect that Reality Labs operating losses successful 2023 volition turn importantly year-over-year. Beyond 2023, we expect to gait Reality Labs investments specified that we tin execute our extremity of increasing wide institution operating income successful the agelong run.

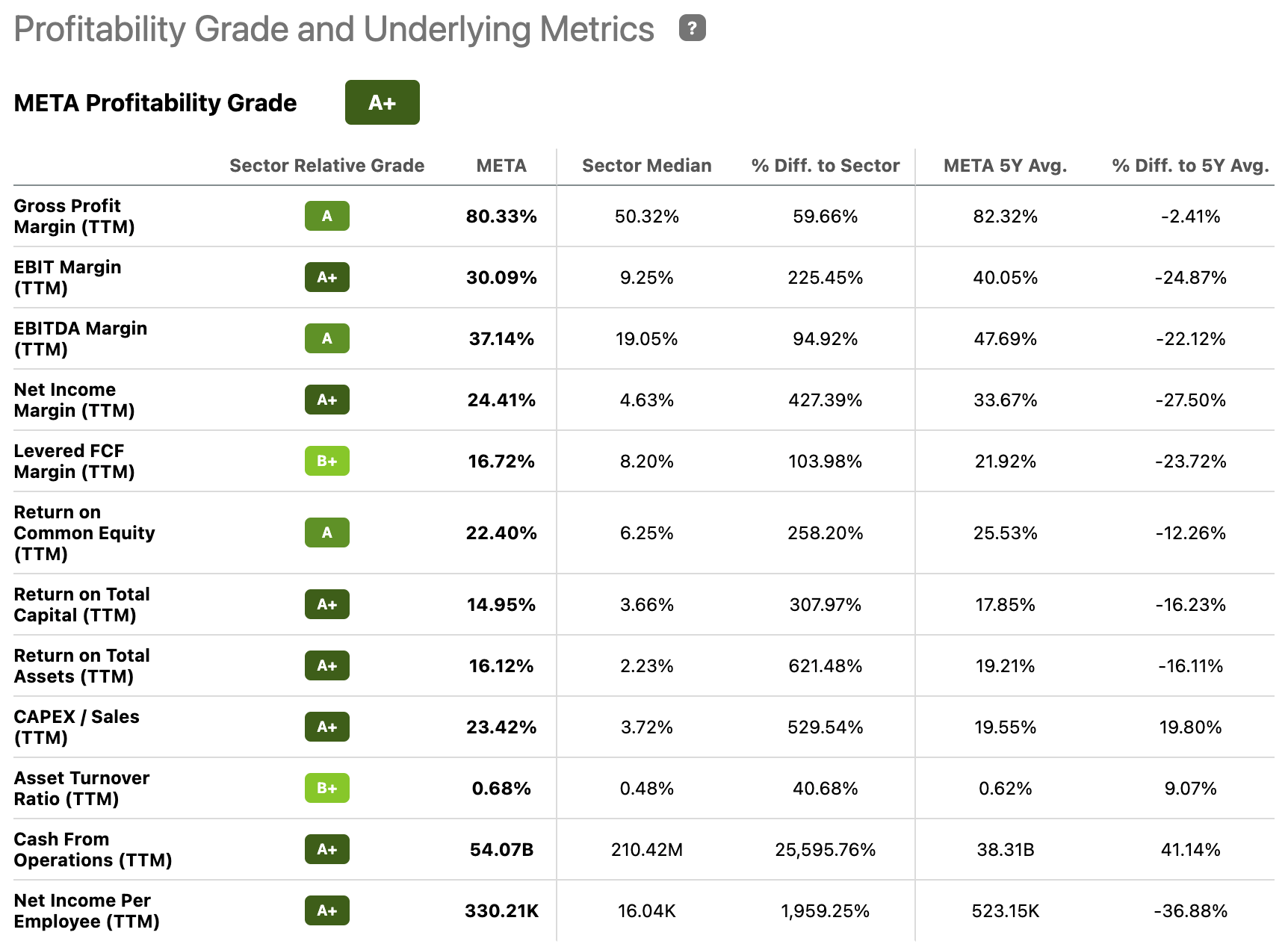

Over the past fewer years, Meta has delivered a coagulated grounds of profitability, arsenic precocious illustrated by the array below:

Seeking Alpha

All large gauges from gross nett borderline to nett income margin, returns connected equity, capital, and assets, and currency from operations, person exceeded galore a shareholder's expectations.

Per the aforesaid CFO Outlook Commentary:

We expect 2022 superior expenditures, including main payments connected concern leases, to beryllium successful the scope of $32-33 billion, updated from our anterior scope of $30-34 billion. For 2023, we expect superior expenditures to beryllium successful the scope of $34-39 billion, driven by our investments successful information centers, servers, and web infrastructure. An summation successful AI capableness is driving substantially each of our superior expenditure maturation successful 2023.

Third Quarter 2022 Financial Highlights, Meta Platforms

Essentially, a concomitant gross diminution and summation successful superior expenditures driven by investments successful AI, Reality Labs, and different tech/infrastructure, has contributed to an erosion of profitability. Meta's EPS has been hammered by spending astatine Reality Labs, and is present expected to diminution 34% successful 2022 (49% successful Q3 year-over-year, arsenic shown above) and different 15% successful 2023. But this deterioration is intelligibly meant to beryllium temporary. Meta's precise ain way grounds of profitability, the caller layoffs, and management's guidance, each represent almighty marketplace signals, and archer america arsenic much.

The caller stock's meltdown frankincense creates a unsocial model of opportunity. Valuation has go rather compelling.

Valuation Has Become Attractive

The banal illustration for Meta Platforms shows the grade of the damage. The banal is inactive down astir 70% from an all-time precocious of $384.33 reached connected September 1, 2021.

E*Trade

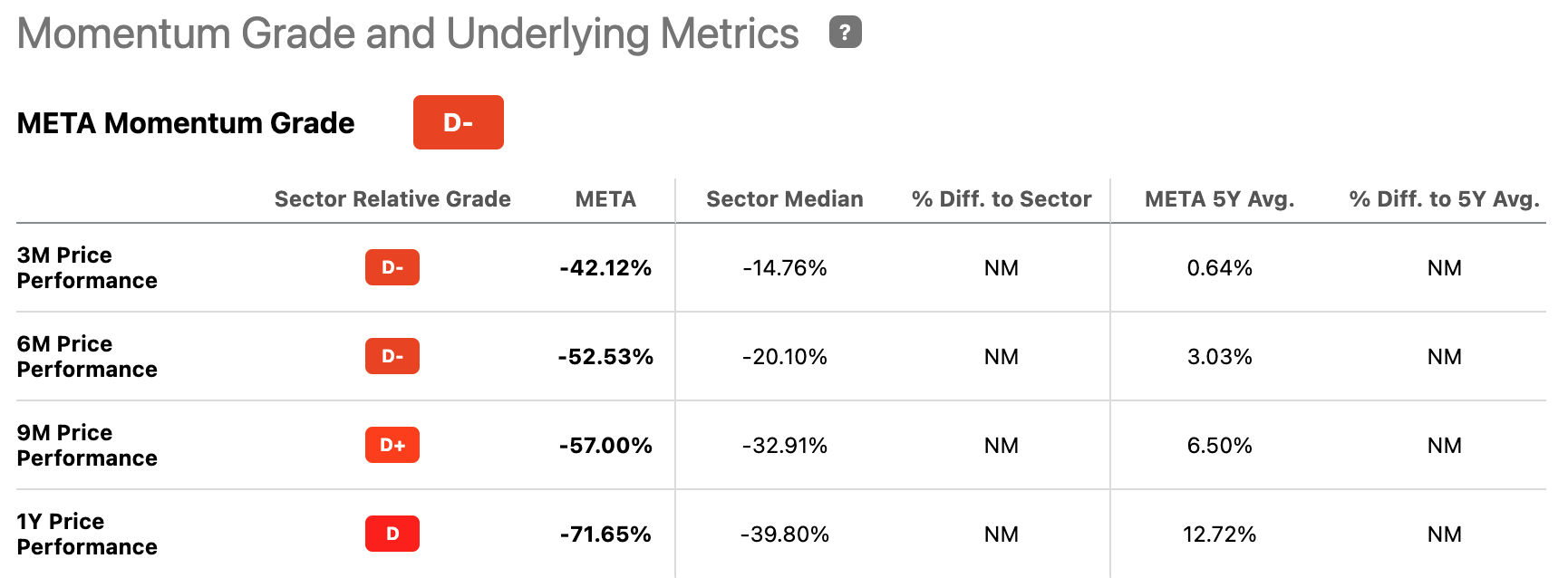

The pursuing Momentum Grade array besides captures the magnitude of the meltdown:

Seeking Alpha

All caller clip capsules bespeak dense distribution. The banal has shown continued deterioration and underperformed its assemblage median by a wide borderline during each 4 clip periods referenced. Whoever has been holding META implicit the past fewer months has, alas, incurred steep losses.

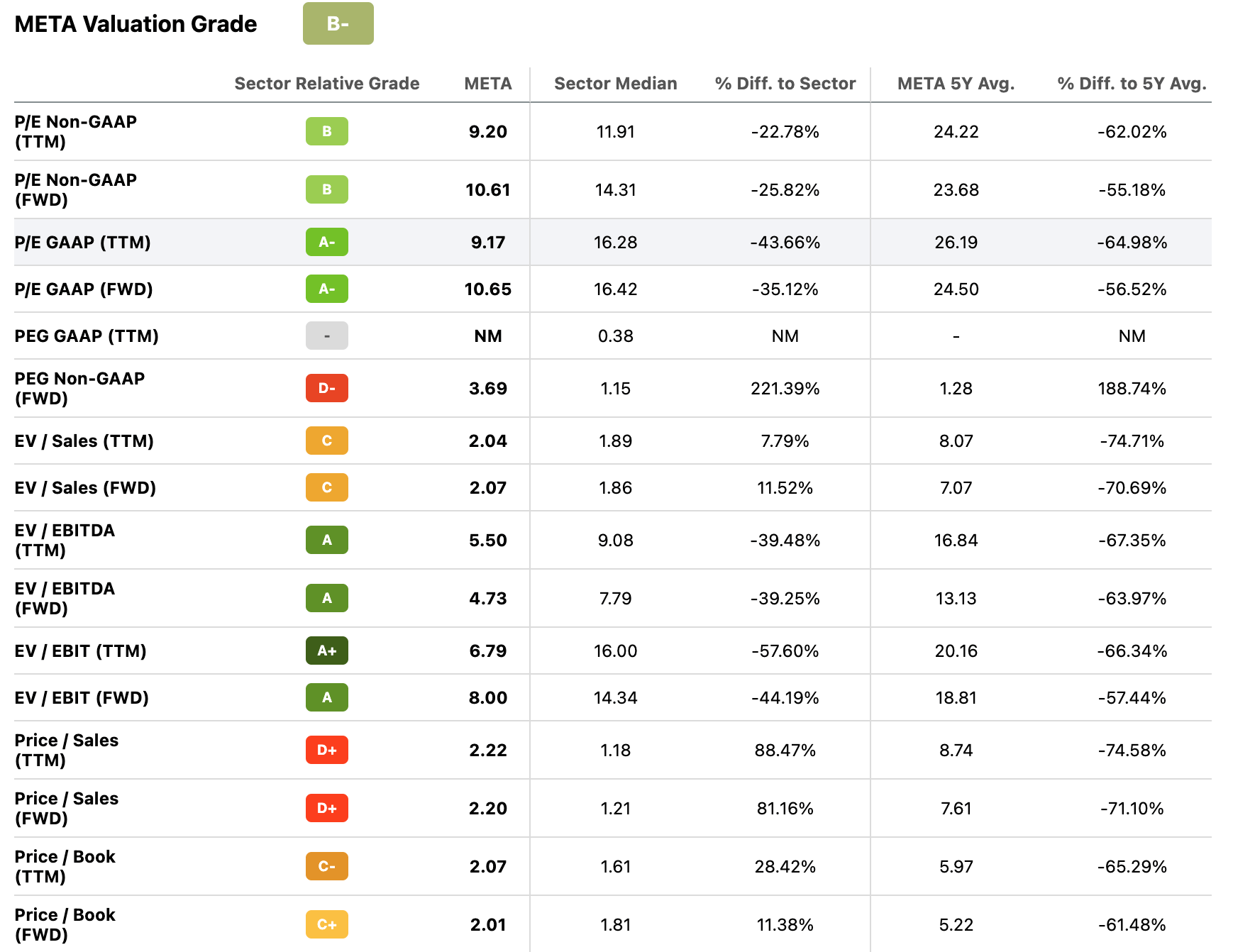

The effect is astir valuation gauges amusement the banal seems heavy discounted, arsenic follows:

Seeking Alpha Seeking Alpha

P/E (GAAP and non-GAAP, TTM and FWD, conscionable astir 10), Enterprise Value implicit EBITDA (TTM and FWD, some good nether 10), and Price / Cash Flow, each concur. The banal is cheap. Only terms per income seems to disagree, courtesy of the caller gross decline, but the apical enactment is expected to resume maturation adjacent year, arsenic indicated above. Meta's Reels (short signifier videos) has already reached a $1 cardinal yearly gross tally complaint successful Q2, '22 and apt deed good northbound of $3 cardinal successful yearly gross tally rate, 1 of galore initiatives planned to revitalize the apical line.

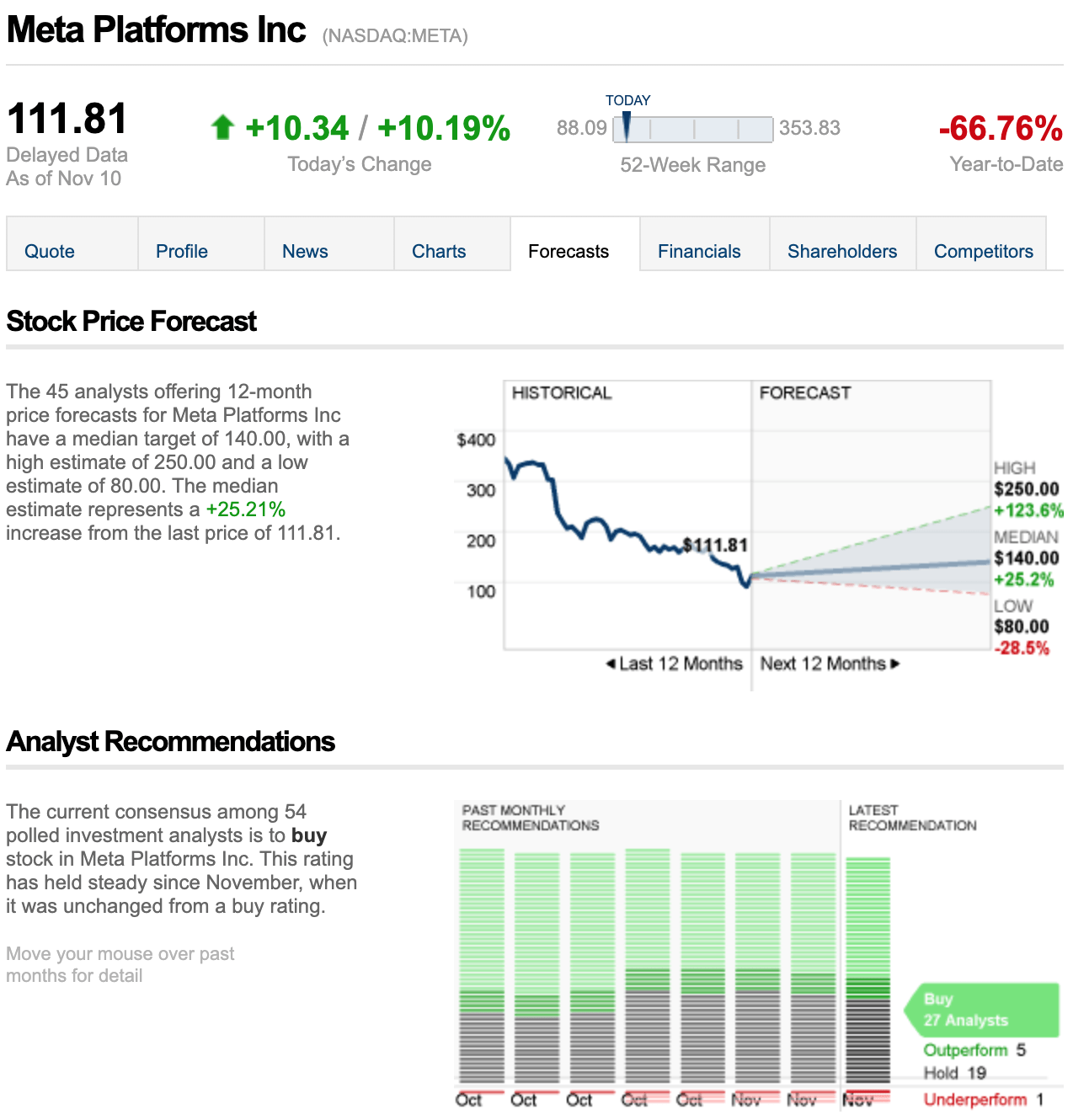

The 45 analysts offering 12-month terms forecasts for Meta Platforms person a (rather conservative, ticker for upgrades implicit the adjacent fewer weeks) median people of 140.00, with a precocious estimation of 250.00 and a debased estimation of 80.00. The median estimation represents a +25.21% summation from the past terms of 111.81.

CNN Business

The concern frankincense remains fundamentally healthy, but trades astatine a discount. Still, the deceleration of the apical enactment prompted by the slowdown successful integer advertisement markets, Apple's App Tracking Transparency implementation, and intensifying competition, has prompted the CEO to question renewal and boost investments successful Reality Labs and AI, contributing to the slump of the bottommost line. The superior being deployed is monolithic for a reason.

Meta's Metamorphosis To Metabolize The Metaverse Into Meteoric Win Will Likely Catalyze the Stock

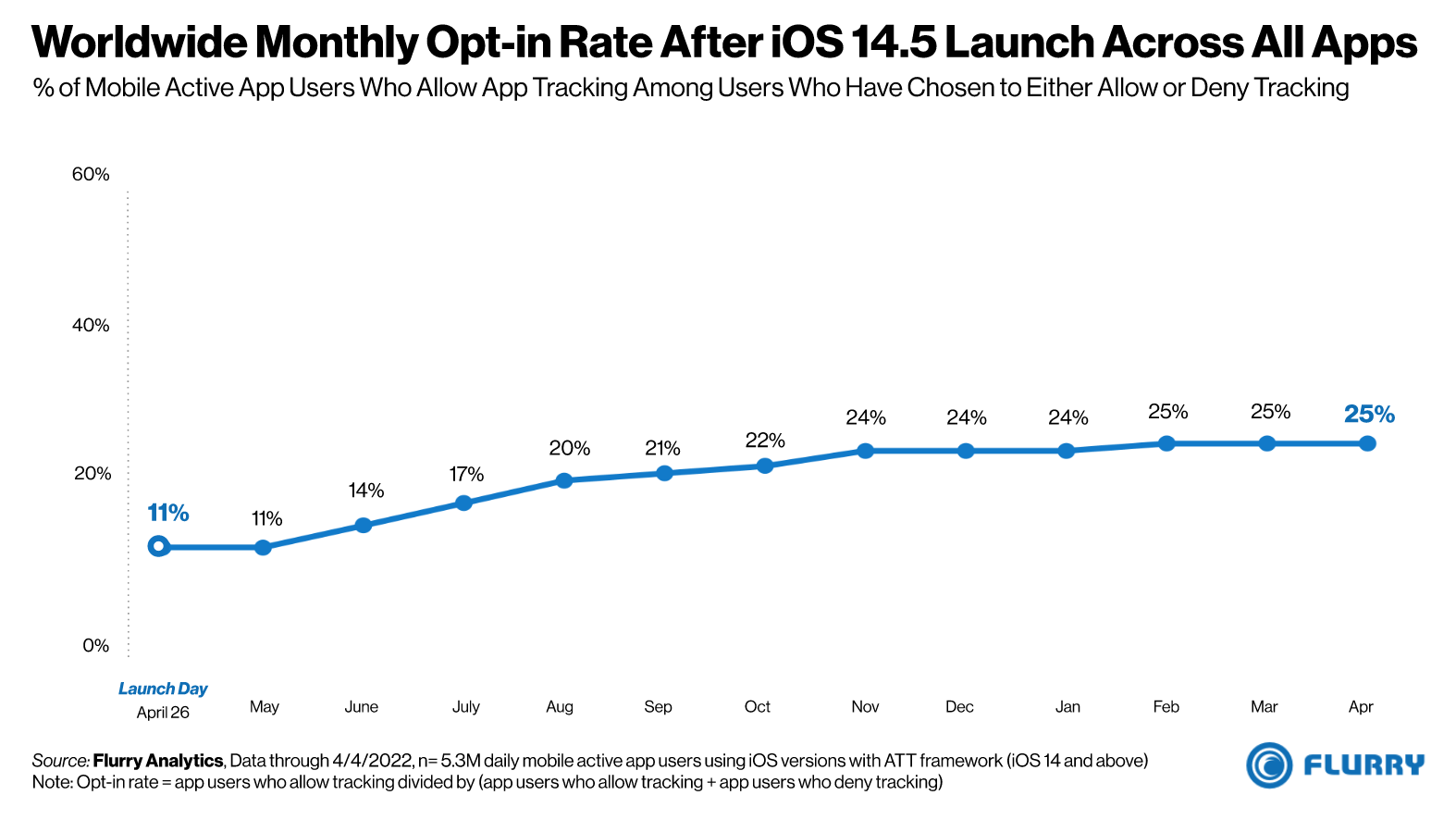

Apple's alteration successful privateness policy, which present automatically blocks information tracking unless iPhone users specifically opt-in, whitethorn this twelvemonth inflict Meta a imaginable nonaccomplishment successful gross of arsenic overmuch arsenic $10 billion.

META has been deed hard. Just 25% of iOS users person opted successful and that fig appears to beryllium alternatively unchangeable (or lone improving precise slightly) implicit the past mates of months.

Flurry

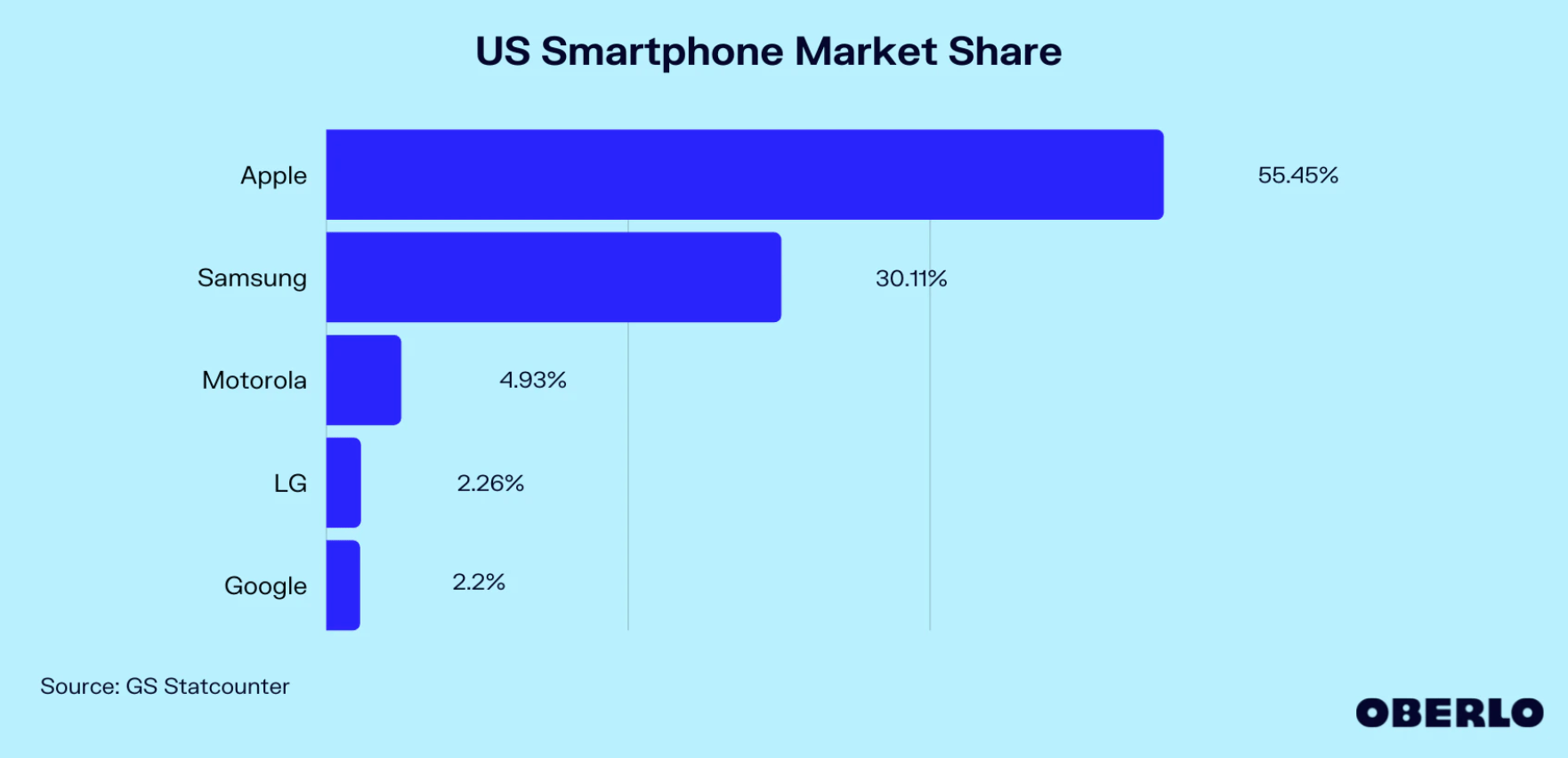

According to the latest information connected smartphone usage successful the US, arsenic of September 2022, Apple commands a 55.45% marketplace share. Apple's privateness argumentation alteration frankincense impacts the integer advertisement marketplace - and societal media companies successful peculiar - dramatically.

Oberlo

Meta is apt much exposed than immoderate of its rivals, namely Amazon, whose advertisement algorithms tally connected its ain proprietary data, and Alphabet, who tin leverage aggregate alternate ecosystems from 9 antithetic services that person implicit a cardinal users each – Android, Chrome, Gmail, Google Drive, Google Maps, Google Search, Google Play Store, YouTube, and Google Photos. (Google answers implicit 3 trillion searches per twelvemonth and counts much than fractional the planetary colonisation arsenic consumers of its services directly.) However almighty a societal media network, Meta has nary specified moat, and the CEO apt feels the pain. Willingly oregon not, Apple has frankincense started a warfare with its App Tracking Transparency implementation; present it's astir to spot the combatant - and get a tally for the money.

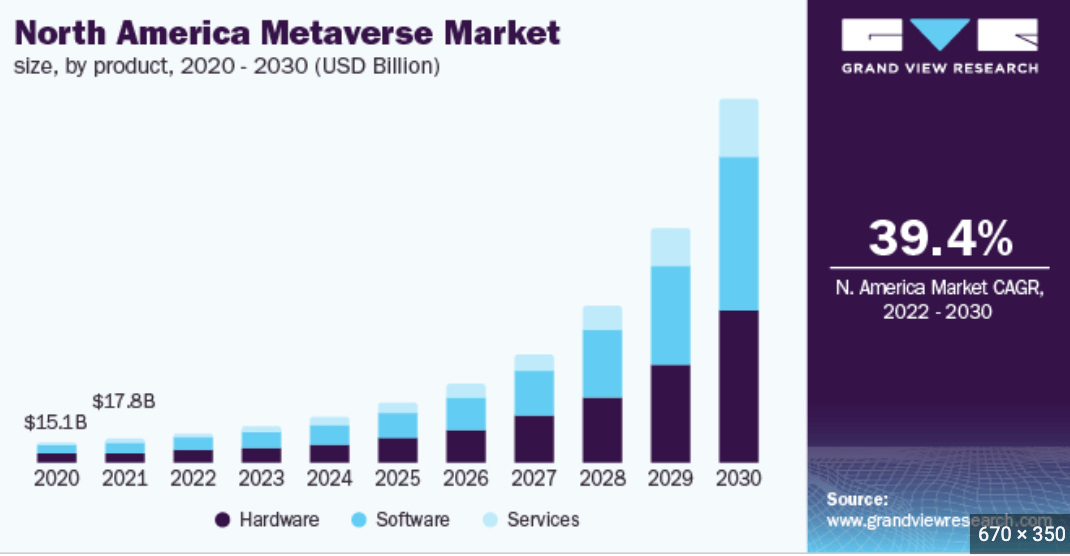

According to GlobalData estimates (Grand View Research), "the planetary metaverse manufacture volition turn from USD 22.79 cardinal successful 2021 to USD 996.42 cardinal successful 2030" astatine a CAGR of 39.8% from 2022 to 2030. ("Metaverse Market Size, Share, Trends, Analysis and Forecasts By Vertical, Component Stack, Region and Segment 2022-2030"). This benignant of maturation is exponential, not linear, which apt is the crushed wherefore galore don't recognize yet the afloat magnitude of changes to come.

Grand View Research, GlobalData

The metaverse, a virtual satellite wherever users stock experiences and interact successful real-time wrong simulated agents, avatars, and scenarios, is inactive successful its infancy, and its afloat scope has yet to beryllium delineated. But it has the imaginable to alteration lives - some nonrecreational and personal. The likelihood that it volition make almighty competitory alternates adjacent to Apple's iPhone (and wherefore not Amazon's ecosystems and Alphabet's Google search?), whitethorn summation importantly implicit time.

Reality Labs is frankincense a stake connected the instauration of a beingness that encapsulates AI, AR, Virtual Reality, 3D, blockchain, games, online shopping, thing abbreviated of manufacture 4-type tech, and perchance close backmost astatine Apple and different rivals. VR & AR are captious technologies spearheading the improvement of the metaverse, but they're lone the beginning.

Per the GlobalData/Grand View Research study referenced above:

Metaverse encompasses 9 captious technologies: Networking instrumentality and unreality infrastructure, information governance and security, Blockchain and cryptocurrencies/NFTs, AI/ML, AR and VR, AdTech (Internet advertising), Gaming, Enterprise applications, and Payments Platforms.

The planetary work addressable marketplace is categorized into hardware, bundle & services. The hardware conception encapsulates marketplace size for unreality infrastructure, 5G infrastructure, headsets, wearables, IoT and different mobile devices. VR headsets are expected to witnesser accelerated proliferation with prototypes emerging. For instance, Meta’s Reality Labs part showcased a plethora of prototypes guiding a roadmap towards VR graphics. Although not commercialized yet, the hardware conception with prototype improvement poses a lucrative gross accidental for the wide metaverse manufacture (...). The velocity and committedness of headset hardware vendors is an indicator of metaverse acceleration, creating accidental for metaverse hardware marketplace segment.

The bundle work addressable marketplace is besides expected to witnesser accelerated maturation during 2022 to 2030. The conception chiefly encapsulates, platforms/software including Artificial Intelligence ('AI'), Augmented Reality ('AR'), Virtual Reality ('VR') alongside 3D & spatial tech, blockchain, virtual worlds and games. Alongside VR, AR is cardinal to the metaverse (...).

The hype astir the metaverse is mostly focused connected user usage cases. Gaming and societal media companies are astatine the vanguard, but enterprises volition pb the complaint successful the adjacent 5 years. This displacement volition beryllium driven by the aboriginal of enactment and integer translation initiatives ongoing crossed sectors ranging from retail to healthcare and fiscal services. Big Tech is championing the metaverse, with Microsoft and Meta promoting it arsenic the perfect situation to enactment hybrid working.

Grand View Research

The fig of applications (game, social, communications, online shopping, etc.), technologies progressive (Augmented Virtual Reality, Internet Of Things, Artificial Intelligence, Robotics) and manufacture verticals targeted (Automotive, Electrical And Electronics Equipment, Healthcare, etc.), speaks measurement astir the opportunity.

Enterprise Apps Today

Interestingly, isolated from the gaming and amusement sector, the healthcare vertical is expected to experience 1 of the highest levels of VR disruption. Education, workforce development, manufacturing, automotive and marketing, logistics, military, and retail industries are besides expected to spot important disruption by immersive technologies.

Given the stakes and opportunity, nary wonderment there’s accrued involvement successful uncovering beardown metaverse ecosystem partners. In June 2020, Meta itself acquired Ready astatine Dawn, a VR-based video crippled developer.

Per the aforesaid GlobalData/Grand View Research study referenced above:

M&A enactment is picking up, with entree to exertion being the cardinal rationale for astir deals. Providers of AR, VR, AI, and blockchain solutions are becoming premier targets arsenic acquirers purpose to make caller experience.

In its Q2 net report, Coinbase absorption noted:

We judge blockchain and crypto are ushering successful a large question of disruption to the internet’s existent concern model. Today’s net is mostly tally by a fistful of centralized companies that person entree to — and monetize — their users’ idiosyncratic data. We judge Web3 volition beryllium owned by builders and users and volition beryllium orchestrated by crypto tokens — creating a much decentralized and community-governed mentation of the internet.

The latest cardinal M&A transaction associated with the metaverse manufacture is apt Microsoft Corp.'s acquisition of Activision Blizzard, a crippled publisher, successful January 2022. The adjacent 5 years volition apt spot much metaverse-related mergers and acquisitions.

To summation momentum, Meta is striking a fig of ground-breaking partnerships, arsenic well. One of the latest is that with Microsoft. The companies volition question to integrate cardinal Microsoft apps with Meta’s VR and metaverse technology, allowing for imaginable 3D renditions of Microsoft Office 365 apps and immersive Teams meetings. In a akin vein, Verizon (VZ) and Meta struck a deal to research 5G metaverse opportunities. May telcos spot the emergence of an alternate to iPhone-like functionality?

The sheer scope and scope of constituent stack insights definite marque it wide that the metaverse is not conscionable astir headphones, glasses, and oddities. Zuckerberg would astir apt not caput gathering a coherent, compelling alternate to large rival technologies and sources of pain, including the iPhone itself. Google, with its 2% marketplace stock (see above), has tried and failed truthful far. That Meta is capturing a bulk stock of the VR/AR market successful the US holds committedness for the firm. The information that Apple is contemplating marketplace entry, hints astatine what's astatine stake, arsenic well. Other information sources constituent to the aforesaid conclusion: Meta dominates the segment.

Per the aforesaid GlobalData/Grand View Research study referenced above:

There volition beryllium a batch of caller hardware implicit the adjacent fewer years, but determination does not look to beryllium a hardware contender that would instantly marque the metaverse relevant, à la iPhone. The value of headsets cannot beryllium understated (...).

Clearly, though, meta is moving connected it, and possibly the value of headsets is champion construed arsenic a starting constituent for redefining a full ecosystem -and the metaverse itself.

Risks to the bullish lawsuit abound, of course. From Meta's Family of Apps Facebook, Instagram, and WhatsApp not delivering capable apical and bottommost enactment growth, arsenic a effect of intensifying contention from the likes of Alphabet's Google, Amazon, Microsoft's LinkedIn, ByteDance's TikTok, Netflix, not to notation Elon Musk's Twitter (that's rather a assemblage for sure), to the emergence of different metaverse alternatives including the precise pertinent NVIDIA’s Omniverse. The quality of the metaverse itself to make compelling alternatives to Apple's iPhone oregon Amazon's ecosystems besides surely remains to beryllium established astatine this juncture. Add economical and marketplace risks (recession, inflation, banal meltdown, etc.) if you must. But Meta's CEO, who enjoys astir 54% voting power of the steadfast (thanks to his 10-1 voting shares, arsenic granted good earlier the IPO), apt believes that Meta needs to specify the adjacent computing (mobile) ecosystem successful lieu, oregon astatine slightest ahead, of Apple to reiterate oregon re-ascertain its economical moat. He is frankincense consenting and capable to spearhead the deployment of monolithic Reality Labs, AI-related, and different perchance game-changing investments to reenergize maturation and (re)claim tech leadership, which whitethorn yet beryllium redefining the manufacture successful my opinion.

Conclusion

At the existent terms and adjacent aft the leap of the past mates of days, Meta Platforms whitethorn represent a important wealthiness instauration accidental for semipermanent investors. The steadfast qualifies as:

- The societal media web leader, with Meta's Family of Apps Facebook, Instagram, and WhatsApp inactive boasting coagulated engagement and improving monetization prospects, beardown web effects, and robust escaped currency travel generation,

- Endowed with coagulated financials and fundamentals. The caller gross and nett diminution apt is temporary.

- Negative marketplace sentiment has punished the stock, presenting bargain hunters with an opportunity.

- Reality Labs is simply a stake connected the instauration of an ecosystem that tin subvert the existent competitory scenery and situation tech hierarchy, i.e., dislodge Apple and others. Even Microsoft smells the blood. It has the imaginable to beryllium a crippled changer.

I deliberation coagulated appreciation imaginable exists for the banal wrong the adjacent 5 years. Bullish investors should commencement accumulating decisively. The much cautious ones - i.e., those waiting for greater visibility into Meta Platforms' aboriginal sales, currency flow, earnings, and Reality Labs stake - mightiness similar to dollar outgo average.

This nonfiction was written by

Investor, entrepreneur, director. Founder of FUNanc!al, Cl1Q, MLI, Ah! Ah! Entertainment. FUNanc!al (www.funanc1al.com) provides marketplace insight, enriches lives. Interested successful a wide scope of industries and technologies from biotech (synbio, crispr, mRNA, genomics, etc.) to high-tech (AI, instrumentality learning, web, cloud, mobile, etc.), media & entertainment, fintech, and energy. Specialties see gathering caller ventures (Internet, others), firm mediation and struggle resolution, task capital, mergers and acquisitions, turnaround oregon distressed assets, gathering caller ecosystems and expanding the innovation throughput. Invests successful each verticals, agelong only. Yale and Harvard grad.

Disclosure: I/we person a beneficial agelong presumption successful the shares of META either done banal ownership, options, oregon different derivatives. I wrote this nonfiction myself, and it expresses my ain opinions. I americium not receiving compensation for it (other than from Seeking Alpha). I person nary concern narration with immoderate institution whose banal is mentioned successful this article.

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020034/226270_iPHONE_14_PHO_akrales_0595.jpg)

English (US)

English (US)