.png) 2 years ago

48

2 years ago

48

Justin Sullivan

Meta Platforms (NASDAQ:META): Pioneering The Metaverse

Website: Facebook.com, Instagram.com, WhatsApp.com, Oculus.com

Current banal price: $130.01

Shares outstanding: 2,687.5 billion

52 week high: $353.83

All clip high: $384.33

52 week low: $122.53

Market cap: $349.4 billion

Net cash: $23.8 billion

Enterprise value: $325.6 billion

Headquarters: Menlo Park, California

Number of employees: 80,000+

Average terms people from analysts: $216.15 (66.3~% upside from existent price)

Introduction:

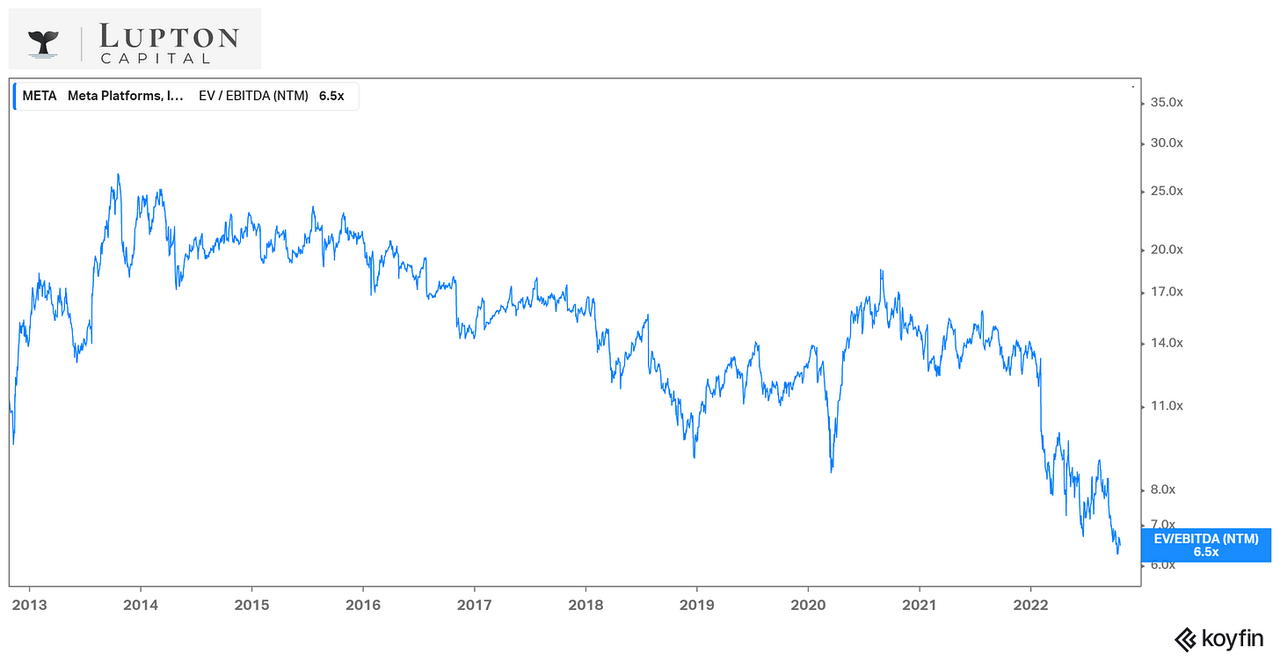

META (formerly known arsenic Facebook) is simply a banal that I get asked astir rather often considering that astir radical are precise acquainted with their products/apps (i.e. Facebook, Instagram, WhatsApp, etc.) but besides due to the fact that the banal is down much than 65% from the each clip precocious (September 2021) and present trading astatine its lowest NTM EV/EBITDA aggregate since the institution came nationalist successful 2012.

I presently person nary presumption successful META; however, fixed the 65% selloff and existent valuation, I'd see 1 successful the adjacent aboriginal but not until we get done net season. I'm decidedly a maturation capitalist and META is nary longer a maturation stock, however, they person the imaginable to beryllium a FCF monster implicit the adjacent fewer years, akin to AMZN and UBER - arsenic capex comes down and FCF margins spell up.

Koyfin

META (personally I hatred this name) has go a inexpensive banal but that's due to the fact that the maturation has disappeared acknowledgment to TikTok, YouTube and different platforms taking immoderate of their marketplace stock (users + advertisement revenue). Between 2012 and 2020, META's revenues grew 42% per twelvemonth (CAGR), but betwixt 2021 and 2026 their revenues are lone expected to turn astatine 8% per year. This is simply a monolithic slowdown and wherefore the banal has been "rerated" (aka aggregate contraction) and present trades similar a worth stock. However, the question present is whether META is worthy buying astatine these prices oregon is this the classical 'value trap' that investors should proceed to enactment distant from arsenic they determination much and much wealth into the metaverse which mightiness not wage disconnected for 5-10 years.

I'm not sold connected the metaverse and I deliberation the banal terms has been partially clobbered due to the fact that different investors are besides not convinced this is wherever META should beryllium investing close now. I judge META is inactive readying to walk $10 cardinal per twelvemonth connected the metaverse which is simply a batch of wealth that possibly could beryllium amended spent connected acquisitions, buybacks oregon possibly adjacent a dividend. I cognize that dividends are a soiled connection for maturation stocks due to the fact that it's fundamentally the institution admitting that maturation is successful the past and present they're going to statesman returning superior to shareholders alternatively than investing for aboriginal growth, but possibly the META committee needs to admit this is nary longer a maturation communicative and it's clip to clasp reality.

The world is that META is simply a currency cattle increasing astatine 8-12% that needs to pull a larger capitalist base, and it's imaginable that paying a dividend could assistance execute this considering determination are thousands of communal funds, ETFs and different types of investors/strategies that lone put successful dividend paying stocks. They mightiness emotion META astatine these prices and multiples but nary dividend means nary position. I deliberation it's clip for META to see changing this. If they implemented a 1.5% dividend, which would beryllium astir $1.95 per stock (not ace appetizing with the 10Y output supra 4% but inactive amended than nothing), it would outgo them astir $5.24 cardinal per twelvemonth (on 2.687 cardinal shares), which is little than 20% of the expected nett income successful 2022. They could adhd a 1.5% dividend and inactive support buying backmost $20 cardinal of banal per year. META has bought backmost an insane magnitude of banal implicit the past mates years (more than $40 billion) and I'd reason it was a atrocious usage of superior considering those buybacks were done astatine overmuch higher banal prices. For instance, META bought backmost $14.5 cardinal of banal successful 2021Q3 and past announced a caller $50 cardinal banal buyback plan. Ironically those buybacks and that announcement each happened with the banal astatine each clip highs. If we spell backmost to September 2021, yields were precise low, wealth marketplace funds were paying nether 1%, truthful a 1.5%-2.0% dividend output from Facebook would person looked beauteous good, though 1.5% of a $350 banal terms would beryllium costing META adjacent to $14 cardinal per year. If determination was ever a clip to commencement paying a dividend it's with the banal astatine 4-year lows.

google

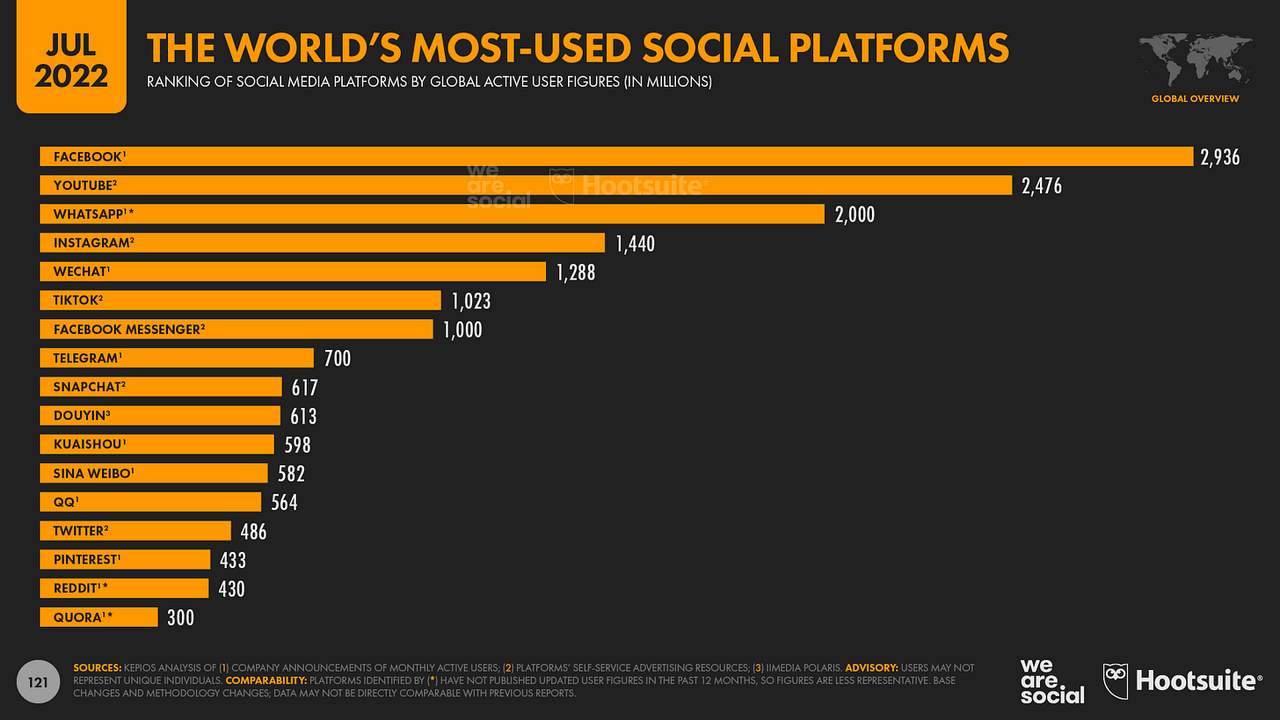

Getting distant from the dividend/buyback argument, META is inactive a beast successful presumption of monthly/daily progressive users and inactive providing a monolithic assemblage for their advertisers nevertheless they person a occupation with idiosyncratic maturation and engagement which is simply a nonstop effect of the emergence successful TikTok. I'd ne'er urge META connected the anticipation that TikTok was banned nevertheless if that really did hap it would astir apt springiness META's banal terms a 30% rally. Same for SNAP (aka Snapchat) and different societal media platforms.

google google

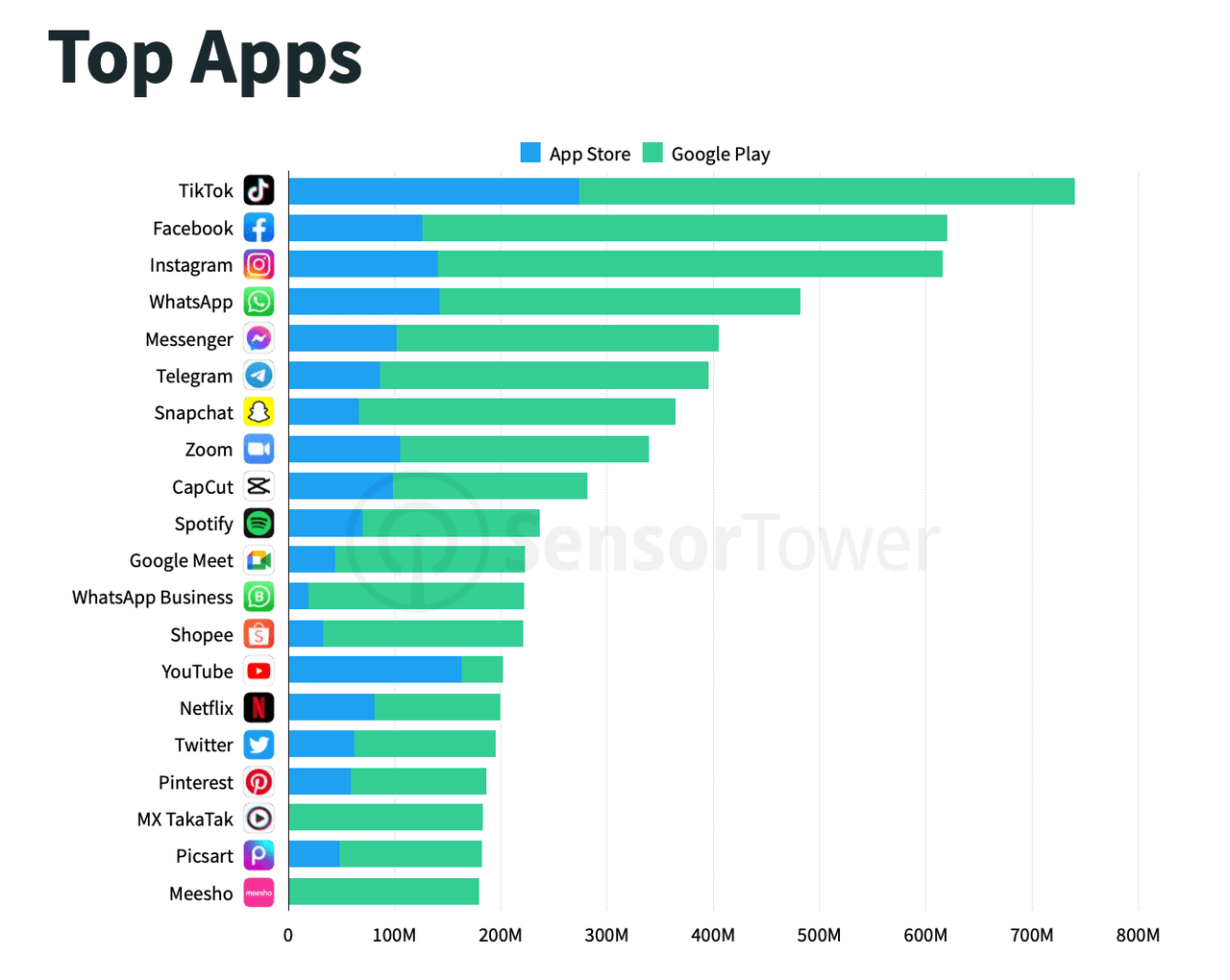

In hindsight, META should person launched Reels overmuch earlier alternatively than letting TikTok go specified a ascendant unit amongst teens and millennials. I bash judge Reels tin beryllium a important merchandise and gross generator for META, but it'll ever beryllium a 2nd enactment to TikTok which is present the astir downloaded app connected a monthly ground according to caller information nevertheless META's 4 main apps instrumentality the adjacent 4 spots which is rather amazing. This leads to my adjacent constituent which is that META needs to bash a amended occupation astatine monetizing WhatsApp and Messenger considering some products person much than 1+ cardinal monthly users.

google

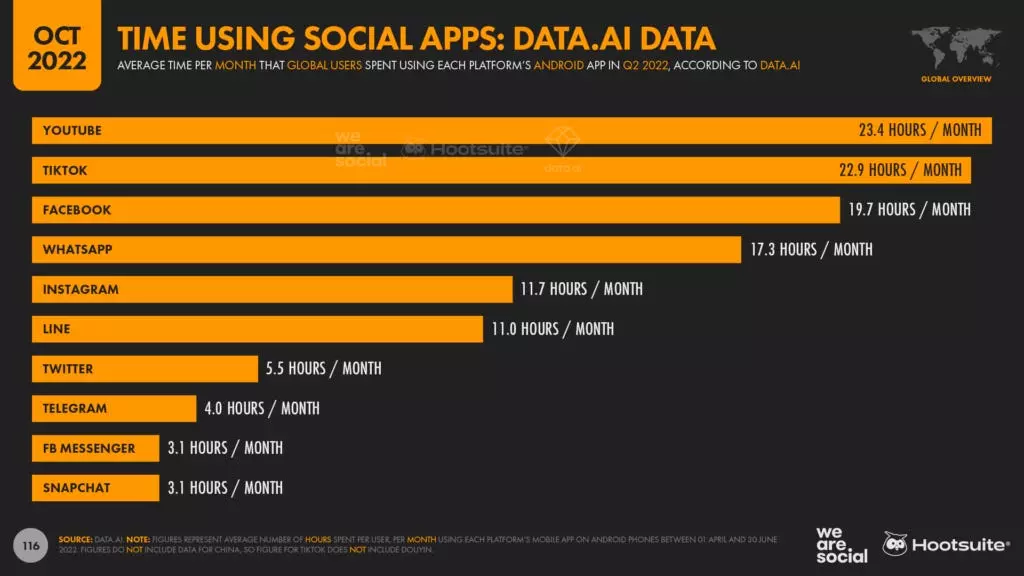

As you tin see, radical are spending a important magnitude of their societal media clip connected YouTube and TikTok, this is not the inclination that META shareholders privation to see. If you look astatine the information narrowed down to kids/teens, TikTok is astir 50% of their societal media usage per time with the different 50% divided betwixt Instagram, Snapchat, Twitter and Facebook. Kids and teens are spending an mean of 75-90 minutes per time connected TikTok.

google

For each the disapproval that Mark Zuckerberg gets (much of it deserved) helium mightiness inactive ain the champion acquisition of all-time erstwhile helium bought Instagram for $1 cardinal successful 2012 erstwhile the institution had little than 20 employees. A twelvemonth agone it was imaginable that Instagram would person been worthy $300 cardinal arsenic a standalone institution but present that tech multiples person travel mode down it's imaginable that fig is person to $150 cardinal which is inactive a 150x instrumentality connected the acquisition price. The lone different deals that travel adjacent to creating truthful overmuch shareholder worth are Google buying YouTube successful 2006 for $1.6 cardinal and eBay buying PayPal successful 2002 for $1.5 billion. All 3 deals would beryllium connected the Mount Rushmore of M&A transactions implicit the past 25 years.

I deliberation galore META investors are consenting to beryllium diligent with Zuck due to the fact that of however good his stake connected Instagram paid off. 10 years agone erstwhile helium bought Instagram astir radical thought helium was insane paying that overmuch for a startup with nary revenues but Zuck had the imaginativeness and it's been a homerun for META but present he's making an adjacent bigger and much costly stake connected the metaverse which is bringing a akin magnitude of skepticism. I bash wonderment however overmuch Zuck truly believes successful the metaverse oregon does helium consciousness pressured to make the "next large thing" for META shareholders?

Summary:

- Largest societal media level successful the satellite that continues monetization wrong advertizing abstraction including; Facebook Shops, Instagram Shopping, Messenger, WhatsApp, and Oculus VR. Supporting extended runway for maturation and monetization imaginable successful Asia and emerging markets.

- Robust equilibrium expanse and escaped currency travel procreation let for enlargement into caller and analyzable visions, specifically the metaverse.

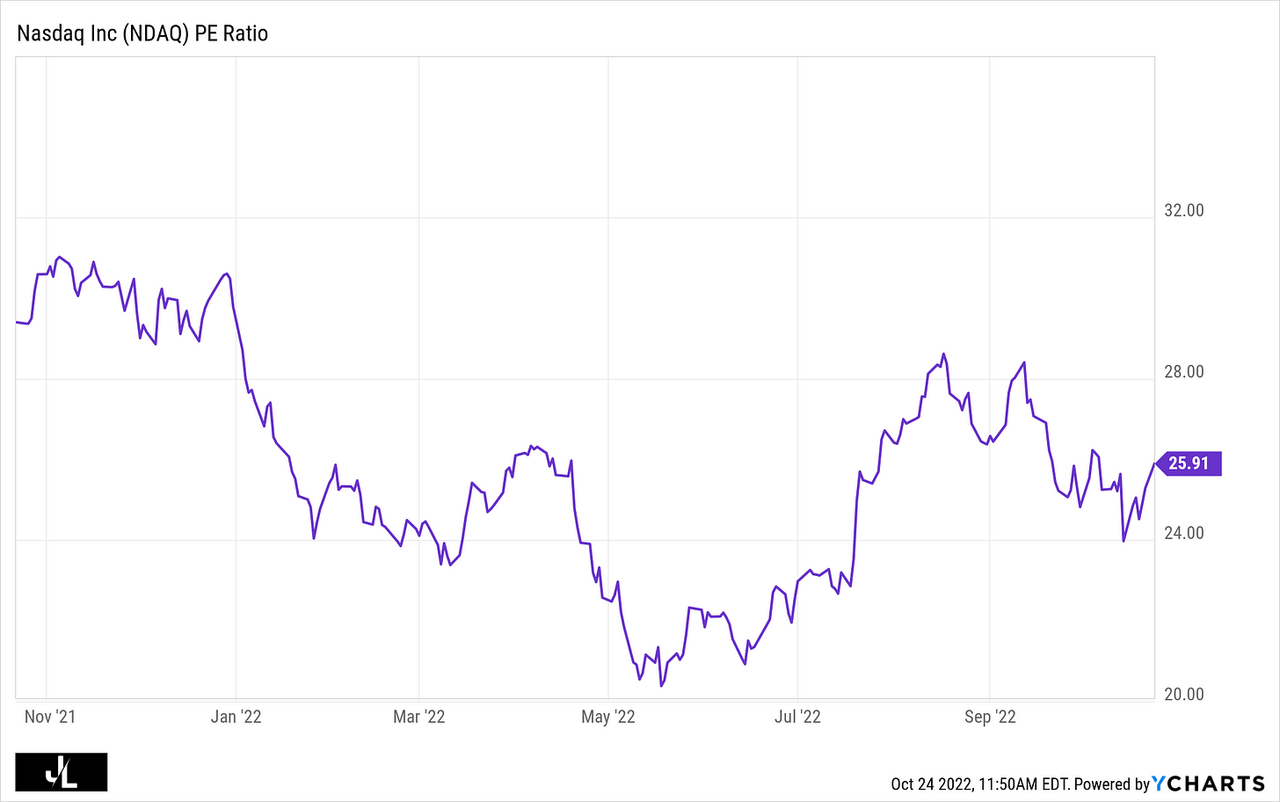

- A heavy weighted tech elephantine successful the Nasdaq that is down astir -61% YTD and -30% successful the past 6 months, trading astatine a P/E aggregate that is 50% little than the mean Nasdaq 100 stock.

koyfin

- The company's metaverse has a semipermanent vision, hence improvement successful this caller abstraction should beryllium thought of successful exponential terms, not linear - nevertheless we won't cognize for galore years whether this metaverse stake is going to wage off.

Thesis: Pioneers successful Virtual Reality

Meta has a first-mover vantage successful a propulsion towards a integer world, specifically changing the mode individuals work, communicate, and create. Q2' net reported R&D expenses of +43% year-over-year, with the bulk contributing to investments successful Reality Labs, which is Meta's augmented and virtual world conception of their business. Expect Meta to proceed deploying billions into Reality Labs, arsenic this is the halfway instrumentality of their metaverse.

The tailwind of Reels advertizing accidental successful the abbreviated term, on with Commerce possibilities implicit the agelong term. Investors bash not needfully person to beryllium beardown believers successful the metaverse communicative to beryllium bullish connected the stock. The archetypal extremity of attaining 1B metaverse users is not overly ambitious, arsenic this would beryllium astir 40% of gamers. Advertising from the institution remains unmatched successful standard and marketer tools compared to competitors (TikTok).

CEO, Mark Zuckerberg is "all in" connected this space, contributing to quarterly profits suffering (-8%, oregon $10.3B). Willing to sacrifice CAPEX to triumph this paradigm shift. From an investor's standpoint, the ROI is hard to value, hence the speculation astir management, and rightfully so.

The Main Theme: Inflection Point and Transition Towards Metaverse

The Metaverse volition yet beryllium inventible, arsenic we germinate from accepted layers of gaming. Examining the originative demolition processes implicit the past fewer decades tin beryllium witnessed beneath based connected the timeline. One indispensable deliberation of the advancements made successful gaming since the aboriginal 2000s and inquire wherefore augmented world and virtual world haven't travel sooner fixed the technological advancements nine is making elsewhere. I judge 3D gaming volition beryllium wherever the idiosyncratic utilizing the controller yet becomes the subordinate himself, hence the metaverse's prominence.

Although determination are respective metaverse platforms specified arsenic Roblox, I judge Meta has the largest competitory vantage owed to 2.8B radical presently utilizing their platform. The question past becomes, however does the institution person the bulk of its consumers to research avenues wrong the metaverse, particularly theirs.

Recent Key Highlights:

Meta's caller woody with Qualcomm to make customized virtual world chips for Meta's Quest devices further highlights the abundant opportunities successful this space, hence the strategical partnership. This besides reaffirms Meta's committedness successful improving the company's Metaverse, enhancing hardware and idiosyncratic acquisition overall.

Salesforce concern to integrate WhatsApp with their services, allowing businesses to chat straight with customers from Salesforce's platform.

Looking Ahead:

Meta volition denote Q3' net connected October 26th with expectations that gross volition beryllium level year-over-year astatine $26-28B for the 4th versus the street's statement of $30B. In regards to full expense, the institution expects this fig to summation importantly from $92B the anterior twelvemonth down to expected estimates of $85-88bn, resulting successful a 22% year-over-year betterment chiefly driven by the hiring frost enacted implicit the summer.

From a macro perspective, an wide slowdown would surely enactment tech retired of favor, starring to terms pursuing earnings. Furthermore, the advertizing spending has decelerated not lone from Meta, but from different marketplace dominants wrong the abstraction (MSFT, GOOGL, AMZN), highlighting a statement among Big Tech's superior headwinds successful the adjacent future. However, contempt the uncertain economical backdrop, Meta is good positioned fixed its scalability successful presumption of level and user-friendliness.

Primary Risks:

Meta has continued to beryllium the laggard successful FAANG stocks this year. The archetypal elephant successful the country is TikTok stealing marketplace stock from Meta's idiosyncratic growth, contributing to the wide slowdown successful users. However, Instagram could assistance offset a ample portion of this displacement successful attraction from young adults.

I americium optimistic astir the company's augmented world (AR) and virtual world (VR), though income volition beryllium the communicative here, peculiarly with however the caller Quest Pro sells connected the market. Investors and consumers either bash not afloat recognize what the metaverse really is, oregon are hesitant successful transitioning from Meta's halfway concern exemplary to this caller paradigm. Hence, the company's superior expenditures expanding are a nonstop correlation to investors' uncertainty. This ties into the question of whether fundamentals are deteriorating, oregon does the institution simply request to revitalize its concern exemplary for the semipermanent occurrence of its existence.

Regulatory scrutiny continues to beryllium an overhang connected the institution itself and is reflected successful the existent banal price. Apple's iOS privateness alteration should beryllium baked successful astatine this point, though making it much hard to absorption connected circumstantial users for advertisement targeting.

Valuation:

As noted earlier this is the cheapest that META has ever traded but that's due to the fact that maturation has slowed considerably and the aboriginal is little wide with much contention than ever earlier not to notation a imaginable looming recession which would beryllium atrocious for advertizing walk crossed META's antithetic platforms.

If we worth META connected nett income, the banal is presently trading astatine 12x 2022 EV/NET INCOME and 11.2x 2023 EV/NET INCOME.

If we worth META connected escaped currency flow, the banal is presently trading astatine 15.5x 2022 EV/FCF and 12.7x 2023 EV/FCF.

All of these numbers are mode beneath META humanities multiples but we each cognize wherefore truthful I won't dissect the reasons again.

Currently META looks cheaper utilizing nett income but if they commencement to little capex and get different spending nether power it should pb to higher FCF margins successful which lawsuit META whitethorn look precise inexpensive based connected 2024 and 2025 FCF numbers (possibly sooner).

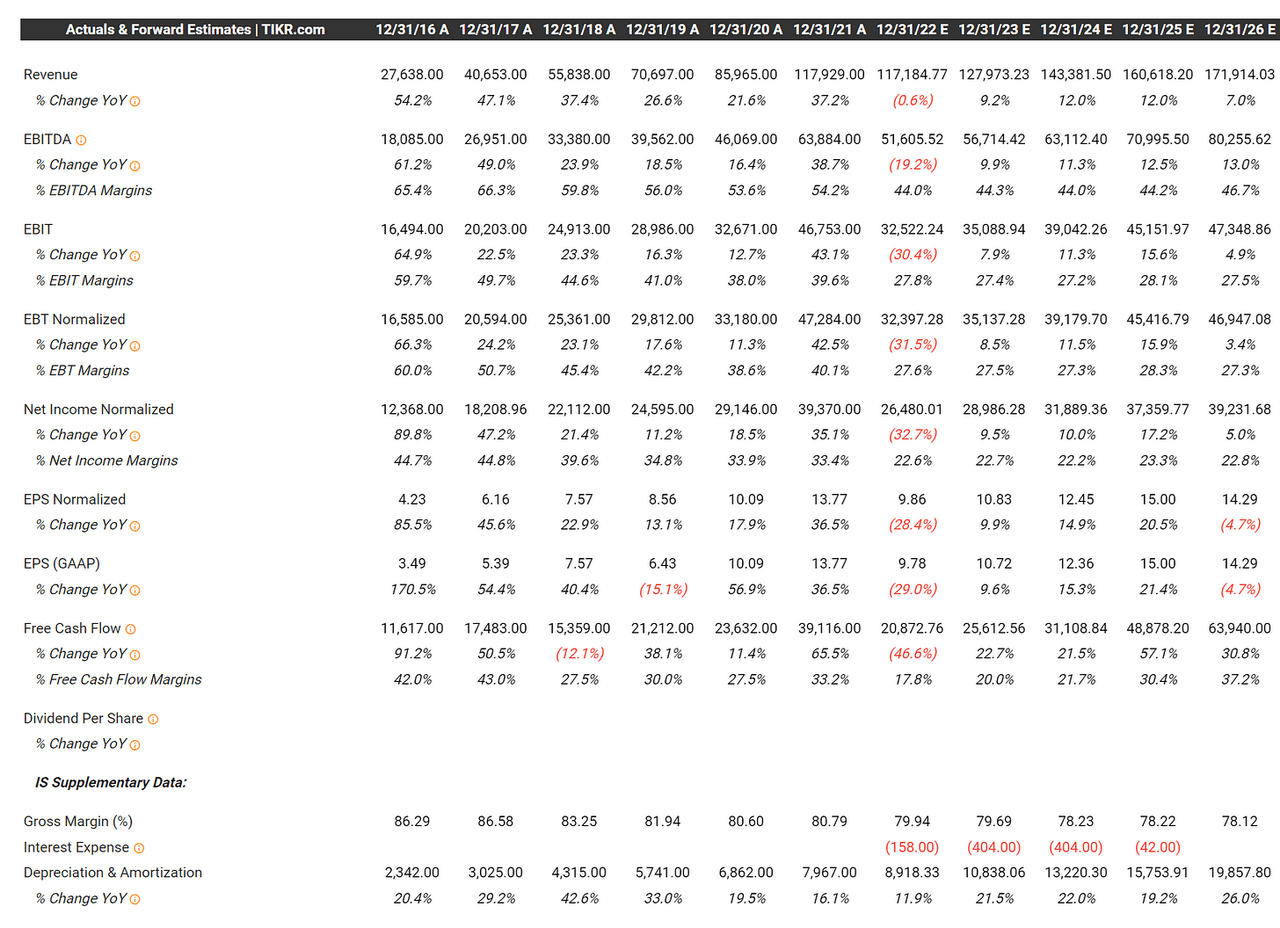

I cognize it mightiness beryllium hard to spot but I included META fiscal information going backmost to 2016 truthful you tin spot however overmuch faster this institution was increasing 5-6 years agone arsenic good arsenic their overmuch higher FCF margins. This is wherever META absorption squad needs to absorption their attraction - they request to get those FCF margins backmost to 35-40% if they privation this banal successful the $300s again earlier this decennary is over.

tikr

Investment Models:

As mentioned above, you tin take to worth META connected nett income oregon escaped currency travel truthful I provided immoderate estimates for both. If you look retired to 2026, assuming the institution tin get FCF margins to 29% (which is beneath the analysts estimates of 37.2%) and you springiness META a 20x aggregate connected FCF past adhd backmost the currency (assuming nary banal buybacks - evidently this is not close but it's intolerable to forecast) and presume 4% banal dilution (which gets them to 3.27B shares successful 2026) past I'm coming up with a ~$368 terms people successful 2026 which is adjacent to the all-time-high from past September.

Lupton Capital concern models Lupton Capital concern models

Technicals:

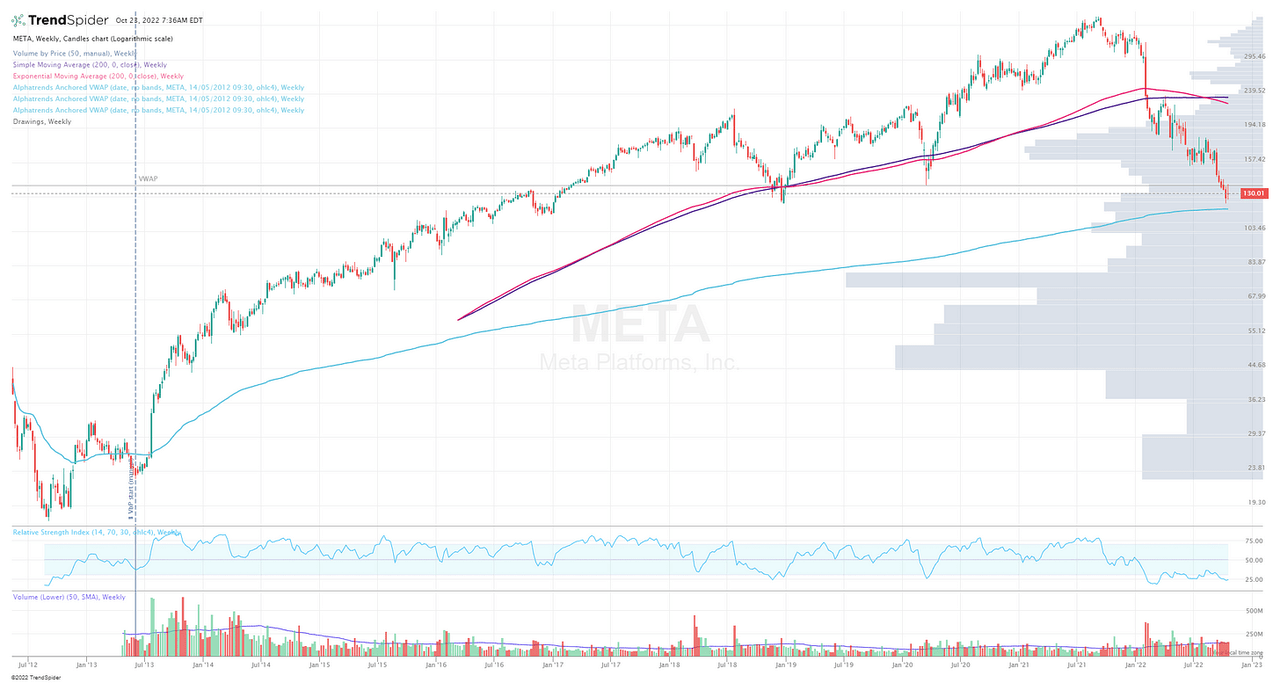

This archetypal illustration shows that META is mode beneath their 200d SMA and 200d EMA but inactive supra the VWAP from the IPO. In information this the closest that META has been to that VWAP since 2013. Just successful lawsuit you're wondering, that VWAP is $118.50 which is wherever I would decidedly commencement a presumption (but usage a halt loss).

trendspider

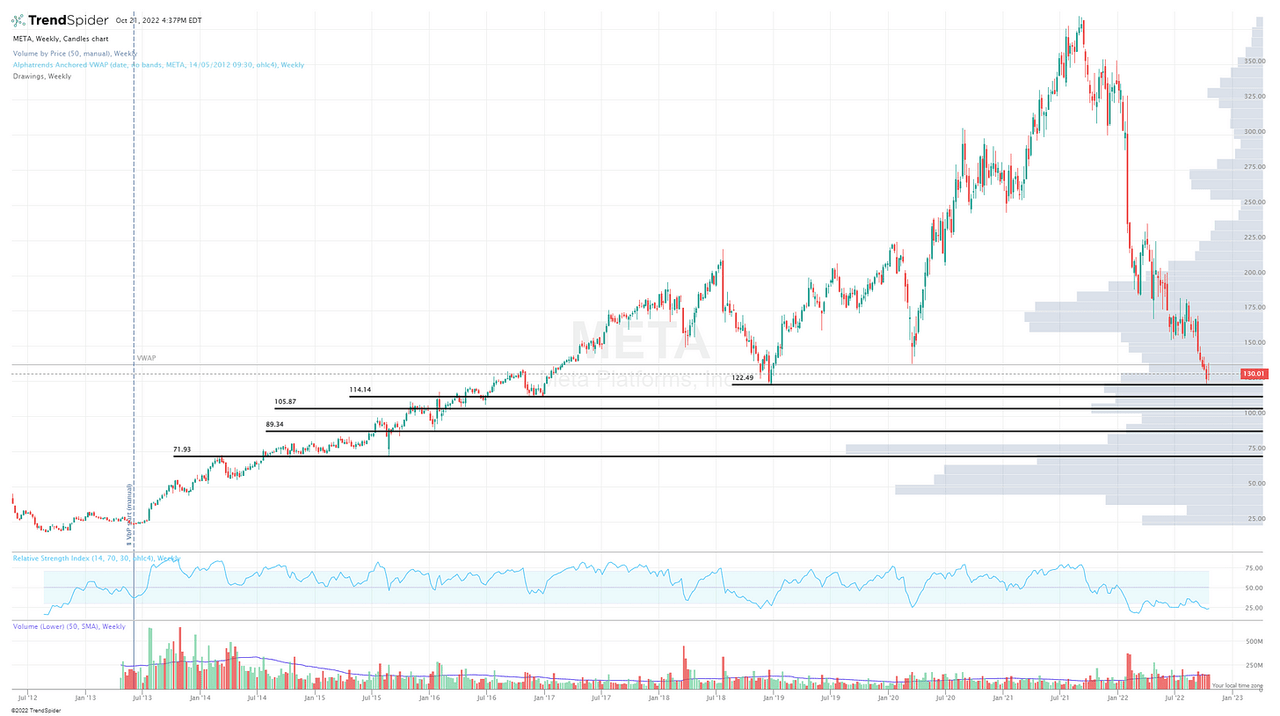

As you tin spot from this adjacent chart, there's decent enactment successful the debased $120s going backmost to December 2018. If that level doesn't clasp up, the adjacent country of enactment would apt beryllium $114 and past $89. Personally I don't deliberation we ever spot META nether $100.

trendspider

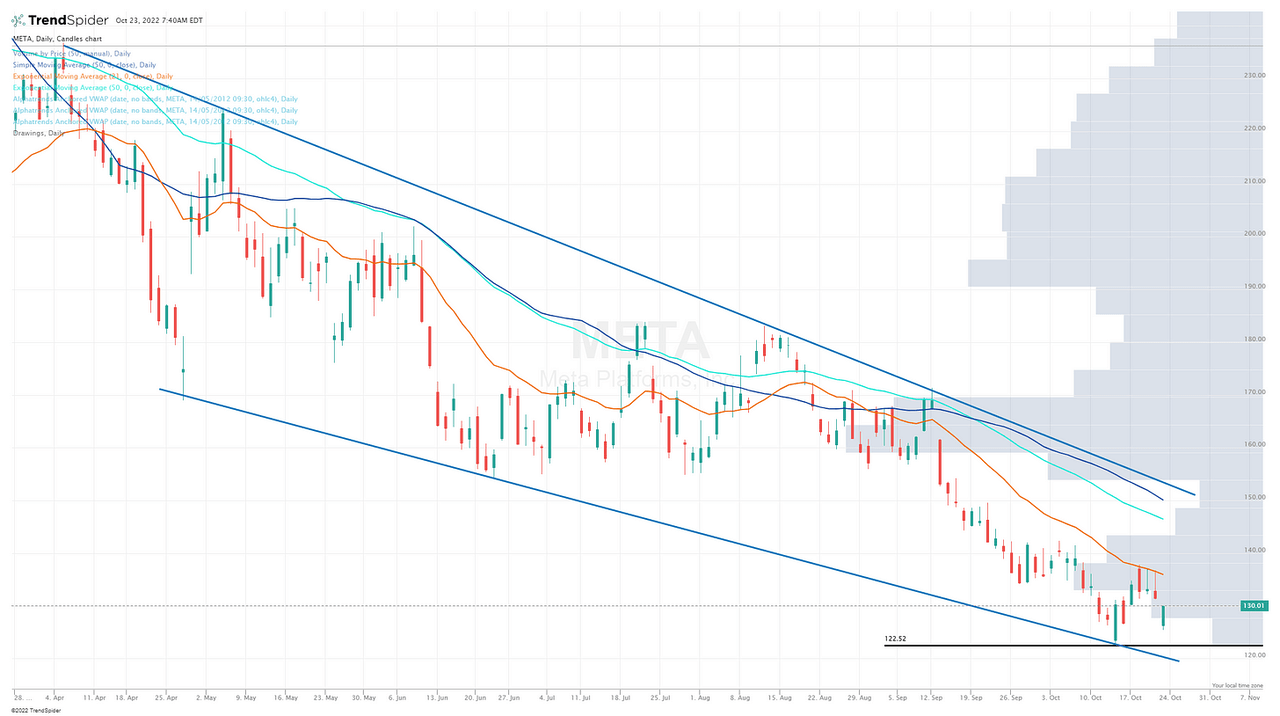

This past illustration is META connected a shorter timeframe chart, arsenic you tin spot the banal has been successful wide downtrend for the past 6 months with precise wide precocious and little bands to this channel. If META can't clasp that $122 level from precocious 2018 it's precise imaginable we spot a bounce disconnected the bottommost of this transmission which mightiness beryllium astir that $114 enactment terms from December 2016.

trendspider

Conclusion:

Like I said astatine the opening of this writeup, I don't person immoderate presumption successful META, but I'm getting tempted to commencement 1 particularly if there's immoderate anticipation of TikTok being banned successful the US. That would beryllium an tremendous catalyst for the banal price.

Whether oregon not TikTok gets banned, I bash deliberation META tin make affirmative returns for shareholders implicit the adjacent fewer years fixed their monolithic idiosyncratic basal (3-4 cardinal radical crossed each of their apps) and tremendous nett margins which volition hopefully summation from present arsenic the institution cuts down connected spending, lowers capex and begins to absorption connected generating much escaped currency flow. If META tin get those FCF margins to 35-40% implicit the adjacent 3-4 years than I judge the banal has a changeable astatine tripling from present and getting backmost to the each clip highs.

I besides deliberation META needs to see immoderate acquisitions. I deliberation Shopify (SHOP) would beryllium a nary brainer (that banal is down -84% from the highs) but I uncertainty it would ever hap due to the fact that the controlling SHOP shareholders would apt ballot against it and/or the US regulators would astir apt artifact it. Assuming SHOP is simply a no-go, I deliberation Pinterest (PINS) would besides marque alot of consciousness and aforesaid goes for Spotify (SPOT). Both of which person go much mature platforms with slowing maturation but monolithic idiosyncratic bases.

Hope you enjoyed this writeup connected Facebook/Metaverse, if you person immoderate questions astir this writeup oregon immoderate erstwhile writeup, delight don't hesitate to scope out.

Are you looking for prime maturation companies to maximize semipermanent returns?

I tally a premium work called Disciplined Growth Investor on Seeking Alpha Marketplace, wherever my squad publishes in-depth probe connected prime maturation companies to compound returns implicit the agelong term. The work besides includes quarterly net analysis, buy/sell trading alerts, my idiosyncratic portfolio updates, unrecorded chat, and overmuch more.

Join a free 14-day trial present and get entree to 10+ heavy dives connected the astir promising prime maturation companies for 2022 and beyond.

/cdn.vox-cdn.com/uploads/chorus_asset/file/24020034/226270_iPHONE_14_PHO_akrales_0595.jpg)

English (US)

English (US)